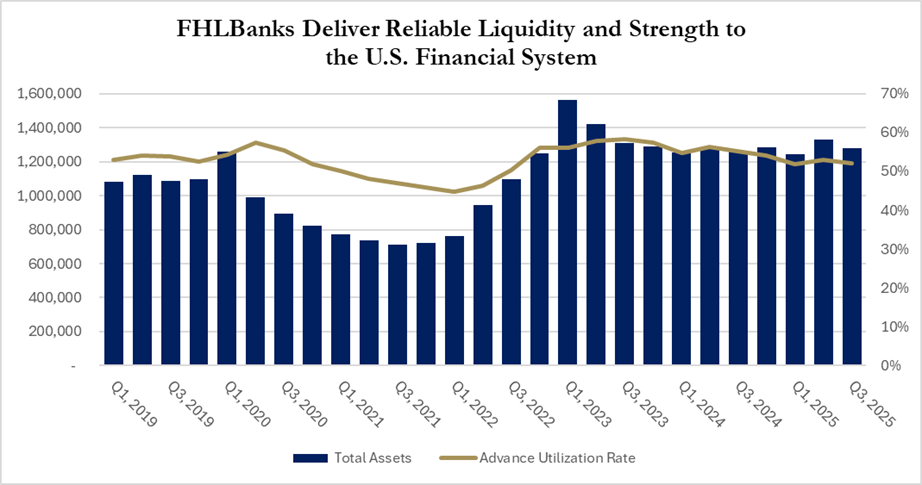

Figure 1: FHLBank Total Assets and Advance Utilization

Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial Reports

Figure 1: FHLBank Total Assets and Advance Utilization

Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial ReportsThe economic environment in 2025 has been marked by heightened uncertainty, fueled by a transition between presidential administrations, shifting policy priorities, and questions about how these changes might impact the broader economy. All of these factors contributed to the Federal Reserve’s decision to pause monetary policy adjustments for much of the year. Uncertainty further intensified with a looming federal government shutdown as the third quarter drew to a close.[1]

On November 13, 2025, the Office of Finance released the FHLBanks’ Combined Financial Report (CFR) for the third quarter of 2025. As shown in Figure 1, from 2019 through the third quarter of 2025, the FHLBanks were a consistent source of stability and liquidity for their members and the broader U.S. financial system—providing the fuel local lenders need to power and invest in communities across the country.

At the end of Q3 2025, total System assets stood at just over $1.28 trillion, with more than 52% of FHLBank members utilizing advances for liquidity.[2] The third quarter marked the 13th consecutive quarter in which more than 50% of members utilized FHLBank advances for balance sheet management or to increase lending and investment in their communities. Over the six-year period shown in Figure 1, advance utilization exceeded 50% every quarter except for the five quarters between 2021 and 2022, when the banking system was temporarily flush with COVID-era cash infusions. The advance utilization rate demonstrates the depth and breadth of support the FHLBanks provide to thousands of cooperative members in communities across the country.

The third quarter featured an unusually U-shaped yield curve. Interest rates were lowest for maturities of roughly four months to seven years, slightly higher for very short-term maturities of one to three months, and highest for long-term maturities of 10 to 30 years. Rates also moved significantly over the quarter—rising throughout July before declining in August and September, as shown in Figure 2.

The yield curve inversion throughout 2025 has continued to challenge traditional financial intermediation models, which depend on borrowing at shorter maturities and lending at longer maturities to earn a positive spread. On September 17, 2025, the Federal Reserve’s Federal Open Market Committee (FOMC) announced its first rate cut of the year, a 25-basis-point reduction that lowered the federal funds target range to 4.0 to 4.25 percent. By the end of the third quarter, interest rates had fallen across most of the yield curve. However, rates for maturities between two and seven years were higher on September 30 than on August 29, underscoring the continued uncertainty permeating financial markets.

Figure 2: Interest Rates in the Third Quarter of 2025 Source: Council of FHLBanks, U.S. Department of the Treasury[3]

Despite the heightened economic uncertainty—reflected in the yield curve and the increasingly divergent views of FOMC members—the stable and reliable liquidity provided by the FHLBanks continued to reassure markets. A report in mid-November by the Urban Institute estimated that the FHLBanks generate between $13.2 and $21.4 billion in annual economic value as a result of their stabilizing presence and dependable liquidity.[4] Similarly, a recent post by researchers at the Federal Reserve Bank of New York recognized that the FHLBanks were created to provide liquidity to their members, support mortgage lending, and provide stability in periods of financial stress, noting that 54% of FHLBank assets—nearly $700 billion—were advance liquidity provided to members and housing associates as of the end of the third quarter.[5]

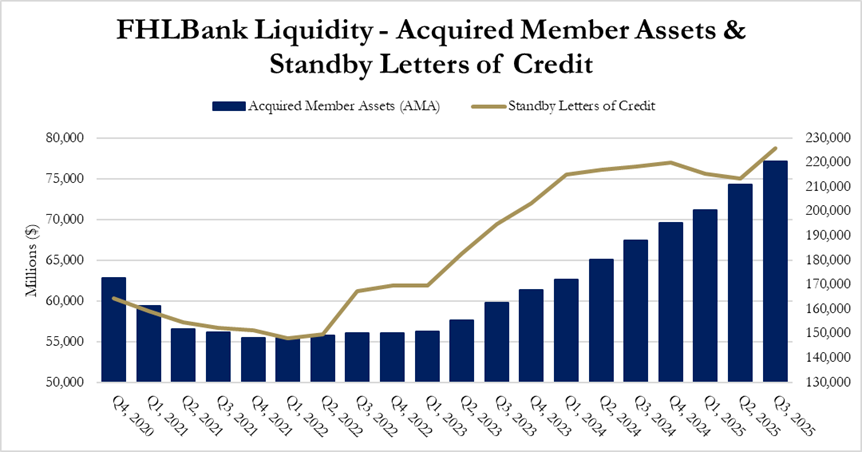

Figure 3: FHLBank Mortgage Purchases and Standby Letters of Credit

Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial Reports

Figure 3: FHLBank Mortgage Purchases and Standby Letters of Credit

Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial ReportsThe FHLBanks deliver liquidity to their members through multiple channels, including advances, standby letters of credit, Acquired Member Asset (AMA) programs, and grant programs such as the Affordable Housing Program (AHP) and voluntary initiatives. The FHLBanks transform illiquid member assets into funding that powers economic activity—construction of new homes, investment in small businesses, and job creation that provides long-term stability for families and communities.[6]

As of the end of Q3 2025, while advances were lower by six percent from the start of the year, liquidity provided by the FHLBanks through AMA purchases, standby letters of credit, and voluntary funding programs all increased. AMA and standby letters of credit rose by 11 percent and three percent, respectively, from the start of 2025, reflecting strong member demand. AHP assessments—statutorily set at 10 percent of income subject to assessment—remained at 10 percent; however, discretionary contributions for voluntary programs increased by nearly 14 percent compared with the same period in 2024.

Figure 3 shows that from Q1 2022 through Q3 2025 liquidity provided by the FHLBanks through standby letters of credit increased by 53 percent, and liquidity provided through AMA programs increased by 39 percent—significant increases that underscore the FHLBanks’ role in ensuring members have access to multiple, flexible funding options so they can reliably serve homeowners, small businesses, and local economies nationwide.

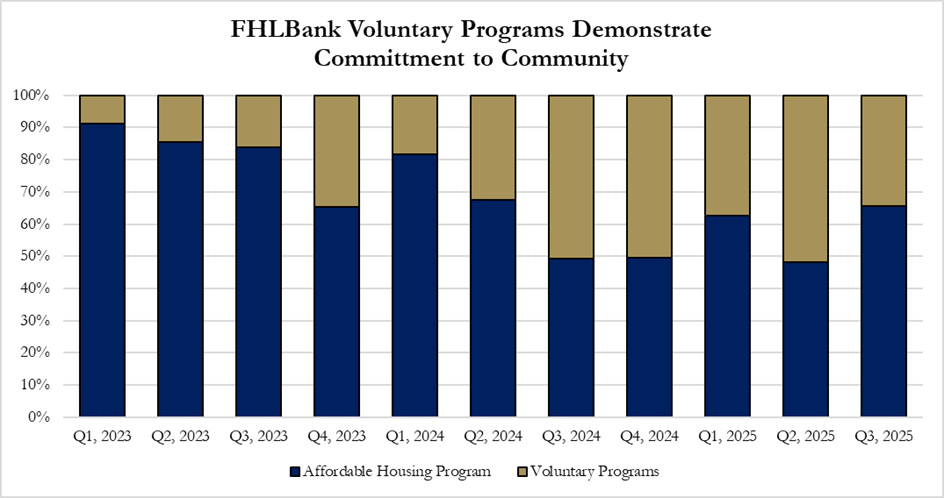

Figure 4: Affordable Housing Program (AHP) and Voluntary Program Expenses

Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial Reports

Figure 4: Affordable Housing Program (AHP) and Voluntary Program Expenses

Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial ReportsThe regional structure of the FHLBank System facilitates the development by each of the 11 FHLBanks of voluntary funding programs tailored to meet the unique needs of their members and the communities they serve.[7] As these programs have expanded, the FHLBanks have increased contributions to support them. As shown in Figure 4, the percent share of grant funding attributable to voluntary programs has grown markedly—from less than 10 percent in the first quarter of 2023 to more than 50 percent in three of the last five quarters. Voluntary program expenditures in the first nine months of 2025 were 13.7 percent higher than the same period in 2024, and, as reported in the System’s 2024 Impact Report, the FHLBanks collectively operated more than 60 voluntary programs in 2024.

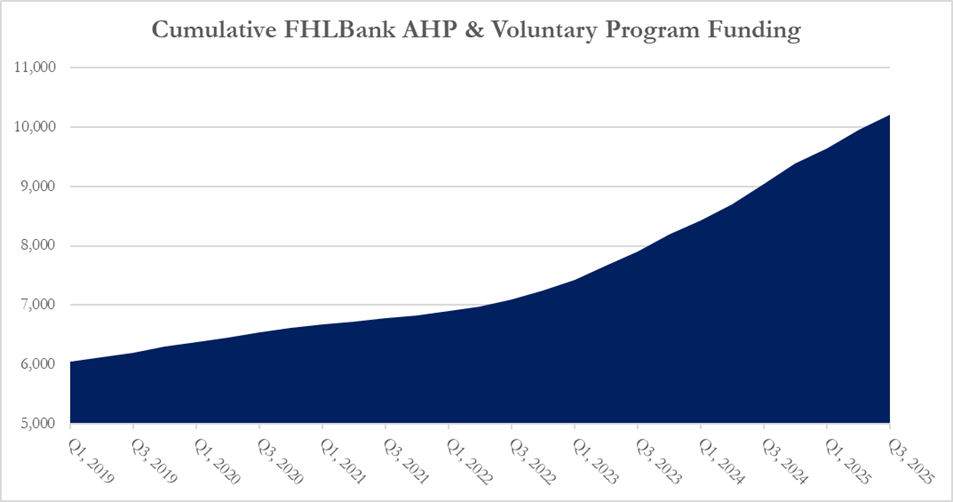

The System’s commitment to voluntary initiatives has increased in each of the last four years. Further, as shown in Figure 5, cumulative AHP assessments and voluntary contributions combined through September 30, 2025, now total to more than $10 billion.[8] [9] This substantial and sustained investment is helping renters, homeowners, affordable housing developers, small businesses, and local communities nationwide. At its core, the FHLBanks’ mission is simple: deliver reliable liquidity that enables members and communities to thrive—and third quarter numbers demonstrate the FHLBanks continue to fulfill that mission every day.

Figure 5: Cumulative Affordable Housing Program (AHP) and Voluntary Program Expenses

Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial Reports

Figure 5: Cumulative Affordable Housing Program (AHP) and Voluntary Program Expenses

Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial Reports

[1] The federal government shutdown from October 1, 2025, to November 13, 2025, was the longest U.S. federal government shutdown on record.

[2] The quarter-end utilization rate likely underreports actual advance utilization during the quarter as it does not account for members that may rely on advances during the quarter but have no advances outstanding at the end of the quarter.

[3] https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value=2025

[4] https://www.urban.org/research/publication/value-fhlbank-system-bank-liquidity-and-stability

[5] https://tellerwindow.newyorkfed.org/2025/11/19/understanding-the-federal-home-loan-bank-system-what-it-is-and-why-it-matters/

[6] At the end of the third quarter of 2025, single-family mortgage loans represented the largest category of collateral pledged to the FHLBanks and over 97 percent of all pledged collateral was real estate backed.

[7] Each of the FHLBanks has designed voluntary funding programs to support housing development, homeownership, small businesses, disaster relief efforts and other initiatives designed to expand housing and local investment efforts. For more on voluntary programs, see the FHLBanks 2024 Impact Report – https://fhlbanks.com/impact-report/.

[8] The Affordable Housing Program (AHP) was created by the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA). FHLBank Affordable Housing Programs have operated since 1990.

[9] Per statute, 10 percent of FHLBank income subject to assessment are assessed quarterly for AHP awards in the following year. Thus, 2025 AHP assessments will be available to fund homeownership and affordable rental housing programs in 2026.