Last fall, the American Bankers Association (ABA) surveyed member institutions on liquidity management and collateralized borrowing. The findings underscore the critical role the FHLBanks play both in supporting community banks and in promoting stability in the financial system. The results are not surprising as they reaffirm recent analyses by the Government Accountability Office (GAO), the Urban Institute, and the Filene Research Institute, all of which demonstrate the importance of the FHLBanks for community lenders in America today.

Last week, ABA published a DataBank article analyzing the results of their Survey on Liquidity and Collateralized Borrowing. This policy brief provides a deeper dive into the survey results.

Routine Liquidity: The FHLBanks as the Primary Partner

The FHLBanks are widely viewed as the single largest provider of collateralized lending to financial institutions in the U.S., with nearly $1 trillion in liquidity outstanding at the end of 2025.

The ABA survey found 67% of respondents use collateralized borrowing on a routine or daily basis.

Figure 1: Respondents That Use Collateralized Borrowing on a Routine or Daily Basis

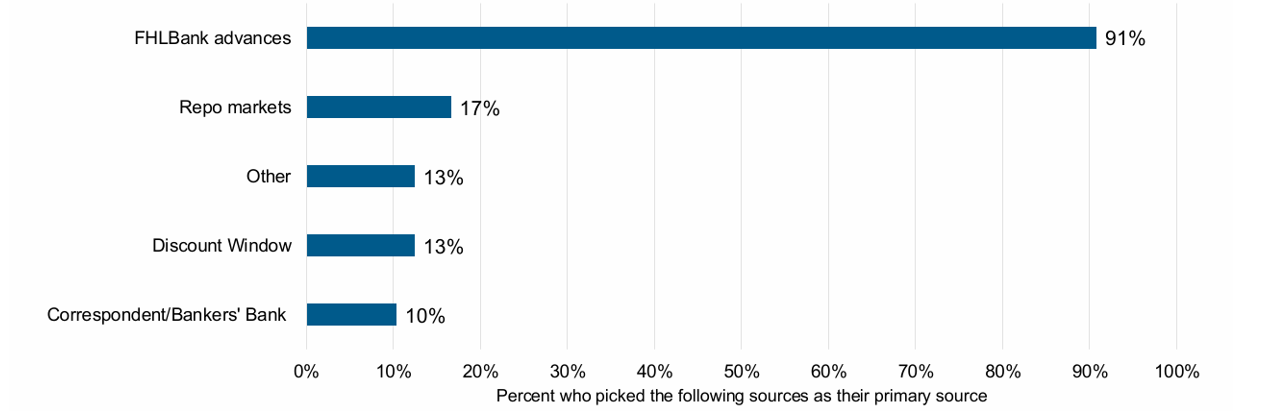

When asked to rank order preferred sources of collateralized borrowing, 91% of respondents indicated FHLBank advances were their #1 choice, while the remaining 9% indicated advances were their second choice. No other source came close to the overwhelming preference for FHLBank advances. Repurchase (repo) markets were the second highest ranked source of collateralized borrowing, with 17% of respondents indicating repo was their top choice, followed by Federal Reserve Discount Window and Other, each with 13% of users reporting those sources were their top choice for collateralized borrowing. This finding clearly demonstrates the preference for the collateralized borrowing products and service provided by the FHLBanks and their central role in meeting member institutions’ routine funding needs. The chart below shows that FHLBank advances were the first choice for collateralized borrowing by a large margin.

Figure 2: Preferred Source of Collateralized Borrowing for Daily or Routine Liquidity

Why Members Choose the FHLBanks

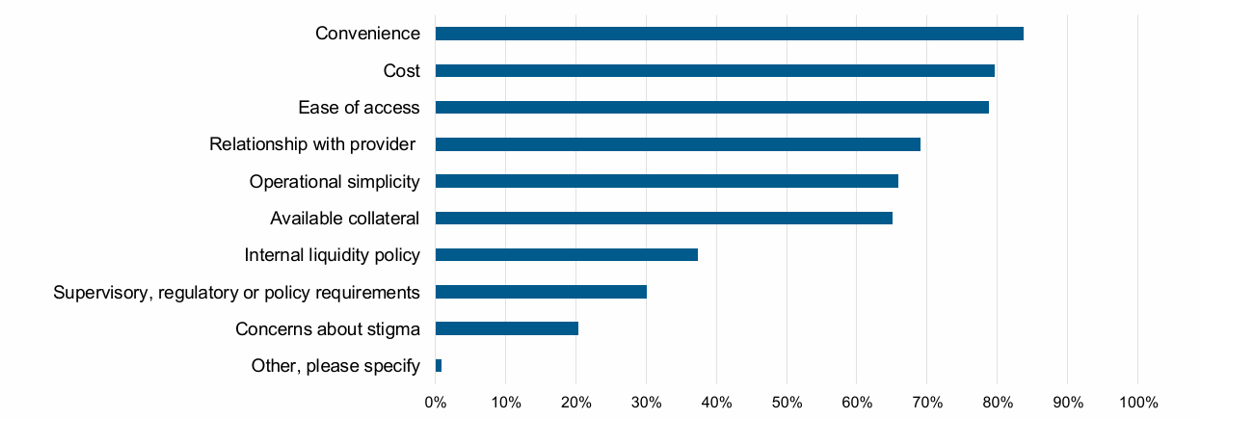

When asked what factors influence a bank’s collateralized borrowing decisions, respondents identified convenience, cost, and ease of access as the top considerations—each a hallmark of the FHLBanks’ cooperative funding model. The fourth most cited factor was the relationship with the provider. The FHLBanks see their members as partners more than customers, recognizing that local financial institutions are the bedrock of their communities, and for nearly 100 years they have built trust and delivered responsiveness through their regional cooperative structure.

Figure 3: Factors Influencing Source for Collateralized Borrowing

FHLBanks: Central to Contingency Funding Plans

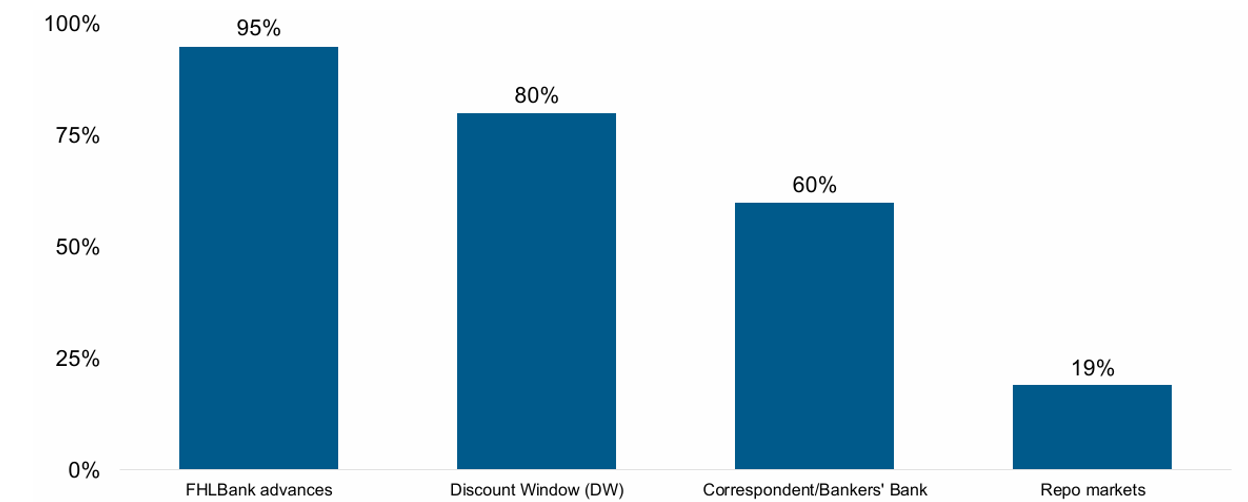

Nearly all respondents—over 95%—reported that FHLBank advances are part of their Contingency Funding Plans (CFPs). These results confirm that FHLBanks are relied upon not just for routine funding, but also for stability in times of market disruption or liquidity stress. The Federal Reserve serves as the lender of last resort; thus, it is not surprising that 80% of respondents indicated the Discount Window is a component of their CFPs. It is also reassuring that 88% of respondents indicated they had completed the process to be ‘Discount Window ready.’ However, being Discount Window ready is not synonymous with using the Discount Window for routine liquidity. In fact, only 36% of respondents indicated having used the Discount Window in the past three months, and 72% indicated they were unlikely or very unlikely to use the Discount Window for liquidity in the next 12 months.

Figure 4: Sources of Collateralized Borrowing Included in CFP

FHLBank Membership and Usage Patterns

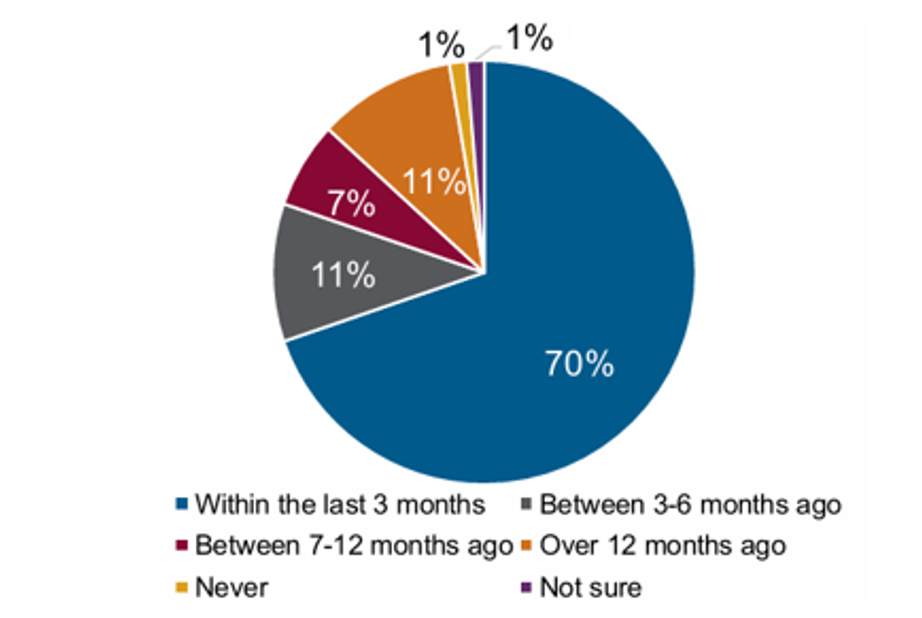

Survey respondents came from all 11 FHLBank districts and nearly all indicated they were FHLBank members. Of community bank respondents, 98% indicated they had used their FHLBank for collateralized borrowing, with 88% indicating they had used their FHLBank in the past year. Accessing FHLBank liquidity for routine purposes was even greater for regional, midsize, and GSIB member banks, with 100% using their FHLBank for collateralized borrowing in the last three months.

Figure 5: When Banks Last Used FHLBanks for Liquidity

FHLBank Liquidity Powers Local Lending and Growth

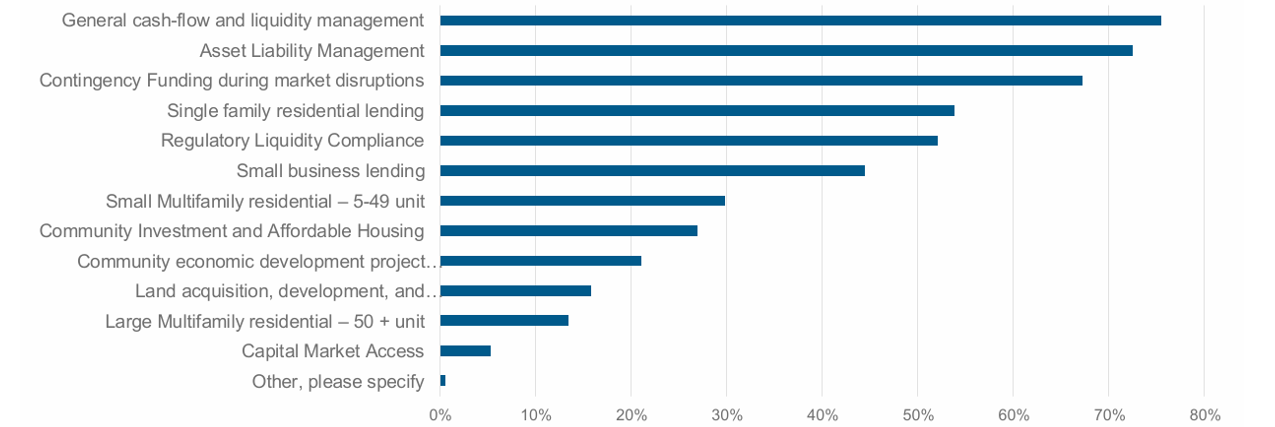

Survey respondents indicated that FHLBank liquidity helped them on multiple levels, with the two greatest use cases being ‘General cash-flow and liquidity management’ and ‘Asset Liability Management (ALM).’ Effective cash-flow and liquidity management are crucial to the viability of community banks, ensuring they can reliably meet funding needs, customer credit needs, and serve as a steady source of financing through economic cycles. Strong asset-liability management complements this by matching funding and lending risks, helping banks remain resilient, safe, and sound, ensuring they can continue supporting local households, small businesses, and community investment. The results in Figure 6 below illustrate the breadth of the FHLBanks’ impact across sectors and communities and confirm the quantitative model results in the Urban Institute’s January 2026 study on how FHLBank liquidity increases lending.

Figure 6: Products Supported or Enhanced by FHLBank Liquidity Tools

In addition to cash-flow and liquidity management and ALM, respondents indicated that FHLBank membership enhances their ability to support customers through expanded offerings – reinforcing the connection between the FHLBanks, their members, and the communities they serve.

Areas of Increased Lending Due to FHLBank Liquidity

-

- Small business lending

- Small Multifamily residential lending – 5-49 unit

- Large Multifamily residential lending – 50 + unit

- Land acquisition, development, and construction lending

- Community economic development lending

- Community Investment and Affordable Housing lending

Flexible Products Meet Diverse Needs

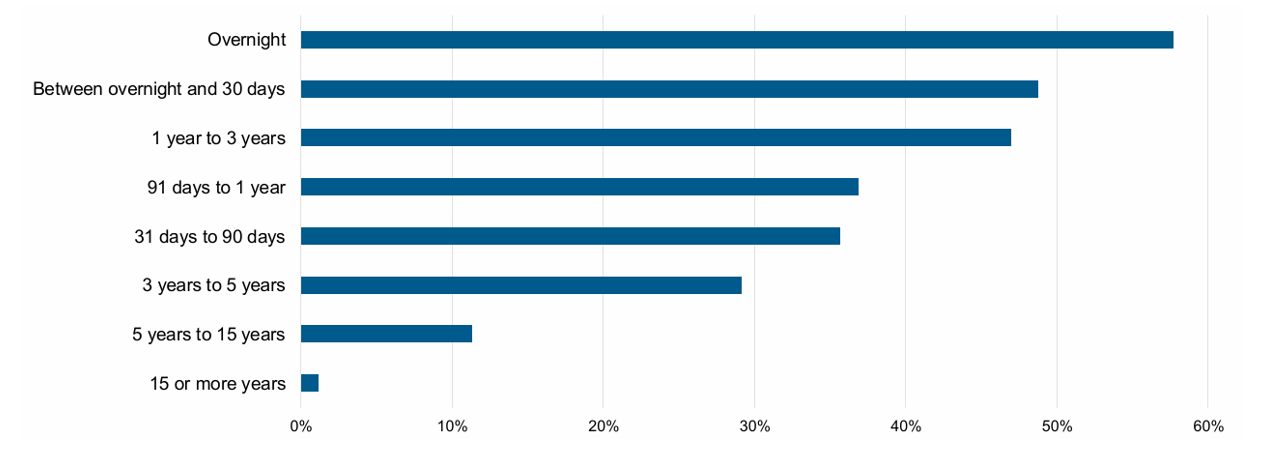

The central mission of the FHLBanks is to provide liquidity to their members to support lending across all economic cycles. The FHLBanks fulfill this mission primarily by providing billions of dollars of advances (loans) to their roughly 6,400 members each day. Other private sector and Federal Reserve liquidity facilities are more limited in scope, while the FHLBanks, as privately capitalized, member-owned cooperatives, offer tailored solutions designed to meet the needs of their members. Survey respondents reported using a wide range of advance maturities, with the top three durations being overnight, 1–30 days, and 1–3 years. This mix of maturities underscores both the flexibility of the FHLBank System and the value members derive from access to a range of terms to meet liquidity needs and manage asset-liability durations. Advances with maturities of 1–3 years, for example, are used by nearly half of FHLBank members and are not available from other liquidity sources, including the Federal Reserve’s Discount Window, which is limited to terms of 90-days or less.

The FHLBanks’ cooperative business model aligns incentives and ensures a mission-driven focus on meeting members liquidity needs rather than executing monetary policy implementation (as with the Federal Reserve) or short-term profit maximization (as with other private liquidity facilities). This helps explain the preference for FHLBank advances relative to other liquidity providers.

Figure 7: Most Frequently Used Advance Terms

Collateral Pre-Positioning and Coordination with the Federal Reserve

Liquidity is the lifeblood of any financial institution. As shown in Figure 1, the FHLBanks are the primary liquidity source for routine, daily liquidity. And as shown in Figure 4, the FHLBanks and the Federal Reserve are the two sources most heavily relied upon in banks’ contingency funding plans. As reported in the latest FHLBank Combined Financial Report, more than $3.7 trillion in collateral was pledged to the FHLBanks. The majority of respondents to the ABA survey indicated having collateral prepositioned at both their FHLBank and with a Federal Reserve Bank. Taken together, these facts demonstrate that the FHLBanks and the Federal Reserve are two pillars of secured liquidity that support the U.S. economy and U.S. financial system.

Given the importance of the FHLBanks and the Federal Reserve in delivering collateralized liquidity to the U.S. financial system, and ongoing efforts at Discount Window modernization, the survey asked participants how to improve collateral coordination. Survey respondents indicated the Discount Window could be improved by adding longer term funding options (similar to what the FHLBanks offer), increasing efficiency of moving collateral between liquidity providers, and standardizing collateral eligibility and reporting with the FHLBanks and other liquidity providers. The FHLBanks support efforts to increase coordination with the Discount Window, as ensuring members have access to reliable liquidity enhances financial system resilience and strengthens the ability of both FHLBank members and non-members to meet the needs of their customers and communities.

On March 13, 2026, President Trump issued an Executive Order titled “Promoting Access to Mortgage Credit.” Among other things, the Executive Order seeks to “modernizing collateral valuation and transfer systems between the Federal Reserve and Federal Home Loan Banks.” In routine times and during times of economic stress and market disruptions, the ability to move collateral and convert high-quality collateral into liquidity is crucial. The FHLBanks look forward to working with their regulator and the Federal Reserve Banks to improve collateral sharing and liquidity provision so that FHLBank members have access to the liquidity they need to provide confidence to customers and financial markets.

Conclusion: Cooperative Liquidity for America’s Communities

The ABA Survey on Liquidity and Collateralized Borrowing provides powerful empirical support for the critical role the FHLBanks play is serving their members and stabilizing the U.S. financial system. Community banks, which make up the vast majority of FHLBank membership, utilize FHLBank advances and other liquidity products to ensure they have the funding they need for both routine operations and contingency liquidity. By providing cost-effective, flexible, and reliable funding, the FHLBanks enable members to serve households, small businesses, and local communities across the country day-in and day-out, regardless of broader market conditions.

Preserving and strengthening the FHLBanks’ cooperative model is critical to ensuring continued stability and reliable liquidity for their 6,400 members, particularly community lenders that anchor communities and expand access to opportunity across the country.

Thank you, ABA, for conducting this important and timely survey.

Appendix

Survey Respondents

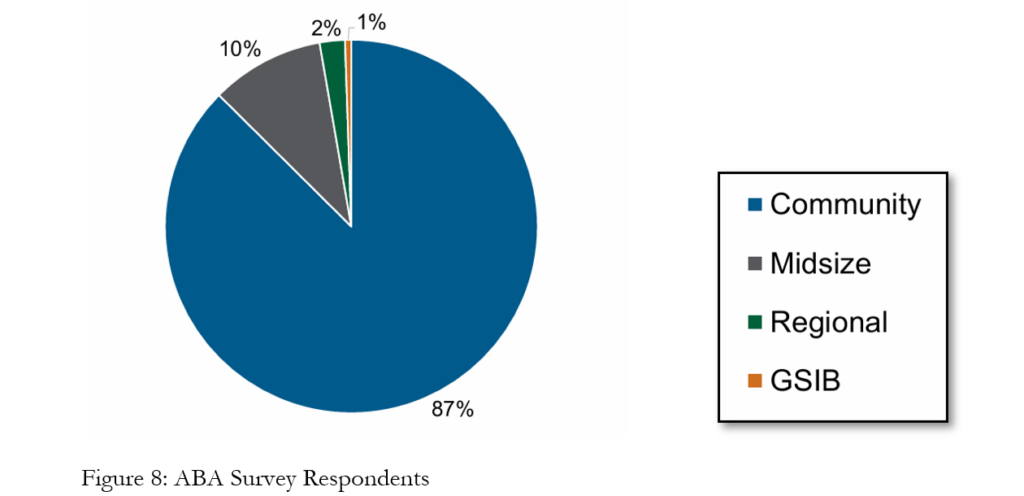

Survey respondents represented institutions across the banking sector but were heavily concentrated among community banks, followed by midsize banks, which aligns closely with the FHLBanks’ membership.

Figure 8: ABA Survey Respondents

References

Brown, Dan, and Aakash Gupta. 2026. ABA DataBank: Inside bank decision-making on liquidity and contingent funding. ABA. ABA DataBank: Inside bank decision-making on liquidity and contingent funding | ABA Banking Journal

Choi, Jung Hyun, Laurie Goodman, and Jun Zhu. 2025. The Value of the FHLBank System to Bank Liquidity and Stability. Urban Institute. https://www.urban.org/research/publication/value-fhlbank-system-bank-liquidity-and-stability

Choi, Jung Hyun, Jun Zhu, Laurie Goodman, John Walsh, Katie Visalli and Bryson Berry. 2026. The Value of the FHLBank System to Promote Housing and Community Development Lending. Urban Institute. https://www.urban.org/sites/default/files/2026-01/Final_The_Value_of_the_FHLBank_System_to_Promote_Lending_0.pdf

Federal Home Loan Banks Office of Finance. 2025. Combined Financial Report for the Federal Home Loan Banks, Third Quarter 2025. https://www.fhlb-of.com/ofweb_userWeb/resources/2025Q3CFR.pdf

Government Accountability Office 2025. Federal Home Loan Banks: Role During Financial Stress and Members’ Borrowing Trends and Outcomes. GAO. Federal Home Loan Banks: Role During Financial Stress and Members’ Borrowing Trends and Outcomes | U.S. GAO

The White House. 2026. Executive Order: PROMOTING ACCESS TO MORTGAGE CREDIT. The White House. https://www.whitehouse.gov/presidential-actions/2026/03/promoting-access-to-mortgage-credit/

van Rijn, Jordan and Caroline Vahrenkamp. 2025. The Value of Federal Home Loan Bank Membership to Credit Unions. Filene Research Institute. https://www.filene.org/reports/the-value-of-federal-home-loan-bank-membership-to-credit-unions