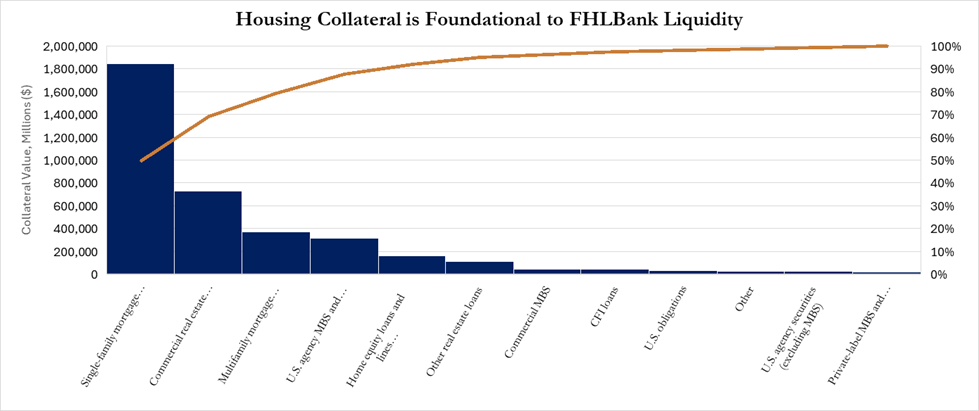

As the above figure indicates, single-family mortgages are by far the largest source of collateral pledged to the FHLBanks. Approximately 50% of collateral is residential mortgages and nearly all collateral pledged to the FHLBanks is backed by housing or other real estate. This demonstrates the core link between FHLBank liquidity and housing finance and underscores a fundamental truth: housing collateral is foundational to the Federal Home Loan Banks’ liquidity mission.

In fact, two out of every three mortgages held on bank and credit union balance sheets are pledged to the Federal Home Loan Banks, supporting liquidity and lending in communities across the country. By comparison, less than 3 percent of collateral pledged to the Federal Reserve discount window is backed by residential mortgages.[1]

Congress chartered the FHLBanks nearly 100 years ago to provide reliable, everyday liquidity to their cooperative member-owners. Since their inception, housing collateral has served as the essential link between the FHLBanks’ and their public purpose of supporting housing finance and community development.

Today, the FHLBanks provide tens of billions of dollars in liquidity each day through fully collateralized advances, standby letters of credit, and other products. FHLBank liquidity allows member institutions to transform illiquid assets—primarily home mortgages—into funding that can be redeployed to meet the credit needs of their communities.

The scale of this intermediation is remarkable.

According to the Urban Institute, banks, credit unions, and other portfolio lenders held approximately $2.7 trillion in residential (first lien) mortgages as of Q3 2025.[2] At the same time, more than $1.8 trillion in single-family residential mortgages were pledged to the FHLBanks as collateral, meaning roughly two-thirds of the residential home mortgages lenders held in portfolio are pledged to the FHLBanks for liquidity.[3]

By helping members convert illiquid housing collateral into available funding, the real-world implications of the FHLBanks’ intermediation becomes clear. Financial institutions across the country that are members of the FHLBank System – roughly 6,400 banks, credit unions, insurance companies, and CDFIs – have access to a reliable funding source that helps them originate new single-family mortgages, fund affordable housing developments, support home renovation and rehabilitation efforts, extend small business credit, and meet the broader financing needs of the families and communities they serve.

Housing-related collateral is the foundation of the FHLBanks’ cooperative liquidity model. It supports lending, strengthens financial stability, and empowers local communities.

The Federal Home Loan Banks remain proud to fulfill their congressionally established mission—provide reliable liquidity, to ensure members have the funding they need to serve their communities through all economic cycles.

[1] https://www.federalreserve.gov/regreform/discount-window.htm

[2] https://www.urban.org/sites/default/files/2026-03/February%20v3.pdf

[3] https://www.fhlb-of.com/ofweb_userWeb/resources/2024Q4CFR.pdf