A recent publication by the R Street Institute, “America’s ‘Other’ GSE Problem: The Federal Home Loan Banks, Part II,” misrepresents the mission, operations, and value proposition of the Federal Home Loan Banks (FHLBanks). While debate about federal policy is healthy and necessary, policy discussions must start on a foundation of facts and proper context. The FHLBanks are cooperative, member-owned financial institutions that support nearly 6,500 member banks, credit unions, insurance companies, and community development financial institutions (CDFIs), and faced with the inaccuracies in this latest article, there is a need to set the record straight.

Liquidity that Strengthens the Financial System

R Street’s article argues that the FHLBanks weaken market discipline and enable risk-taking by financially troubled institutions. This claim overlooks the market discipline built into the fabric of the System and the conservative structure and safeguards inherent in the FHLBank model. The advances (loans) FHLBanks make to their members are fully collateralized, and each FHLBank operates under strict regulatory oversight from the Federal Housing Finance Agency (FHFA). Advances must be backed by high-quality assets, and the cooperative nature of the FHLBank System—with joint and several liability—encourages prudent risk management, not excessive risk-taking. Each FHLBank regularly and actively monitors the financial condition and performance of its members and has access to quarterly call reports and other financial data that members report to their primary regulator. On top of this, the FHLBanks’ Office of Finance interacts daily with capital market participants, raising funds to support advances, mortgage purchases, other liquidity products, and overall system operations. This continuous market engagement serves as a built-in check, embedding capital market discipline at the core of the FHLBank System.

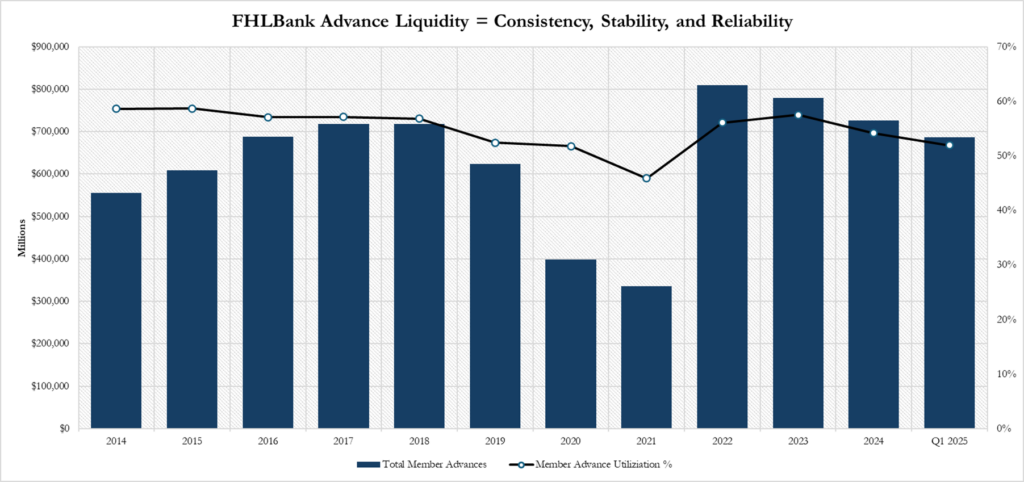

It is important to recognize that making liquidity available to all member institutions is not a flaw—it is the very mission of the FHLBank System. The FHLBanks fulfill this mission successfully under all economic conditions and in times of market stress, when other liquidity sources retreat, the FHLBanks step forward, providing countercyclical liquidity where it is needed most—supporting financial institutions, stabilizing credit flows, and helping markets regain confidence. The R Street article itself cites a 2023 Urban Institute study that concluded “the FHLBs are a source of stability to the financial system, not instability.” During periods of stress, FHLBank members rely on the long-standing relationships they have built with their FHLBank partners—often over decades—relationships that offer a level of familiarity, reliability, and stability not found with other liquidity providers, as shown in Figure 1.

R Street further maintains that extending credit to stressed financial institutions can increase losses to the Deposit Insurance Fund, and ultimately to taxpayers. To support this claim, R Street cites a 2012 working paper from the Federal Reserve Bank of Richmond, which is based on data from 1992–2003. This period is largely prior to enactment of the Gramm-Leach-Bliley Act (1999), prior to the Housing and Economic Reform Act (2008), and prior to the Dodd-Frank Wall Street Reform and Consumer Protection Act (2010). Gramm-Leach Bliley opened membership in the FHLBank System to all commercial banks and strengthened FHLBank risk-based capital requirements. HERA established the FHFA and granted it broader supervisory authority over the FHLBanks than was available to the prior regulator. Dodd-Frank introduced new capital, liquidity, and risk governance expectations for systemically important institutions, which FHFA applies to the FHLBanks.

Applying the findings of Richmond Fed paper to the current operations of the FHLBank System is inappropriate given the intervening legislative changes. Through each of the aforementioned laws, Congress evolved the FHLBank System in significant ways. The System’s core liquidity mission remains, but changes in operations, oversight, and risk management cannot be ignored. One particular change to note is GLBA’s provision allowing each FHLBank to offer different classes of stock with varying risk, reward, and redemption timelines. This embeds strong market discipline by creating real economic incentives for both the Banks and their member institutions to act prudently.

The article cites the March 2023 bank failures as evidence of FHLBank advances imposing increased costs on FDIC, yet GAO’s 2024 report on the 2023 bank runs does not support this assertion. In fact, GAO made very clear in its report that “repayment of FHLBank advances for a failed bank does not impose a direct cost to the Deposit Insurance Fund,” and that FDIC officials noted that FHLBank advances typically represent a small portion of payments during receivership. Further, a 2024 paper by economists at the New York Federal Reserve Bank found that in March 2023, 22 banks suffered bank runs and while two failed, the remaining 20 survived and all did so with funding from the FHLBanks. The research further found that both run-affected and unaffected institutions relied on the FHLBanks to navigate the market stress experienced in 2023. While the 2023 bank failures carried significant costs, costs could have been far higher if more banks failed. The liquidity provided by the FHLBanks to thousands of member institutions nationwide strengthens financial system stability, helps cushion the impact of economic downturns, shortens recovery periods, and supports long-term economic resilience and prosperity.

Figure 1: FHLBank Advances and Advance Utilization Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial Reports

No Government Guarantee, No Taxpayer Funds

The R Street article also repeats the familiar, inaccurate talking point that the FHLBanks rely on federal backing and put taxpayers at risk. FHLBank debt securities explicitly state they are “not obligations of the United States” and are “not guaranteed by the United States.” The FHLBanks are self-capitalizing, cooperatively owned, and do not receive federal (read: taxpayer funded) appropriations. Advances are fully collateralized and FHLBank member private capital is in the first loss position. The FHLBanks’ ability to borrow at favorable rates reflects the System’s nearly 100-year history of conservative financial management, joint and several liability, overcollateralization, and a robust capital structure. If investors assume an implicit guarantee on debt that is explicitly not guaranteed by the federal government, that is their assumption and risk to take—not taxpayers. Moreover, with the System approaching its 100-year anniversary, investors should have a full and clear understanding of the System structure and its embedded protections when determining the appropriate price to pay for debt securities. In other words, investors’ willingness to pay a premium or accept a lower rate of return on FHLBank debt reflects the market’s confidence in the System’s operations and long-standing track record of strong performance. As reported in the System’s Combined Financial Report (December 31, 2024), the FHLBanks ended 2024 with an advance collateralization ratio of more than 5-to-1, that is, the FHLBanks held more than $5 of collateral for every $1 of advances outstanding.

R Street claims that FHLBank members enjoy a “substantial dividend” on their shares, yet the article fails to mention the capital members invest in the System, which is a membership requirement and by statute offers no capital appreciation. The Federal Home Loan Bank Act dictates that ownership shares in an FHLBank are purchased and sold at “par value”. Thus, ownership shares purchased for $100 in 1932, when the System was established, remained redeemable for $100 at the end of 2024. In contrast, a $100 investment in the Dow Jones Industrial Average in 1932 would have grown to over $72,000 by the end of 2024. The FHLBank System is privately capitalized but capital is not free; there are opportunity costs, and in a capitalist economy, investors expect to earn a reasonable rate of return on investment.

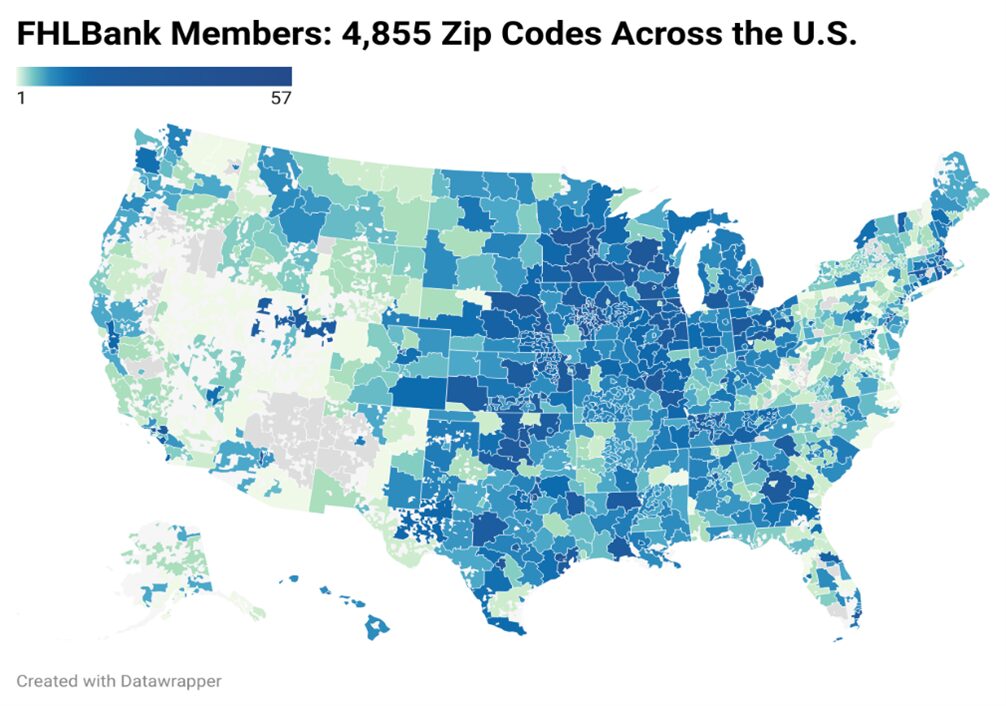

Figure 2: FHLBank Membership

Source: Council of FHLBanks, FHFA

Figure 2: FHLBank Membership

Source: Council of FHLBanks, FHFAA Strong Commitment to Housing and Communities

R Street suggests the FHLBanks have strayed from their mission. The facts tell a different story. The FHLBanks have held true to their mission for over 90 years; however, at the direction of Congress, that mission has been changed and has evolved to meet the changing needs of the U.S. financial system. Throughout the System’s history, liquidity has been the core mission and collateral has been the primary link to housing. The System’s 2024 Combined Financial Report showed that 96.7% of pledged collateral was backed by housing or real estate, mostly illiquid whole loans, that the FHLBanks transform into liquidity that members can use to increase credit availability and support their communities.

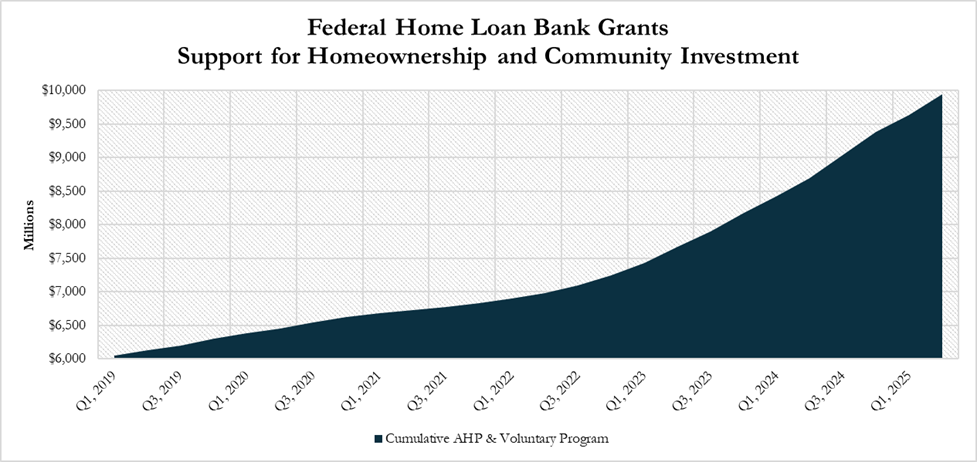

The 11 FHLBanks offer a range of programs to preserve and increase the supply of housing, enhance rental housing and homeownership affordability, and stimulate community investment. In 2024 alone, the FHLBanks contributed a record $1.2 billion to affordable housing and community development through the Affordable Housing Program (AHP) and voluntary programs—reflecting an increase of more than 180% in voluntary contributions from the prior year. That is not mission drift; it is mission delivery.

Figure 3: Cumulative Affordable Housing Program (AHP) and Voluntary Program Expenses Source: Council of FHLBanks, Federal Home Loan Bank System Combined Financial Reports

The FHLBanks’ 2024 Impact Report highlights how AHP funding is being used to support the creation and preservation of more than 26,000 housing units, provide assistance to 17,000 homebuyers, and support thousands of jobs and small businesses in communities across the country. These programs are provided without taxpayer funds and are not found elsewhere in the private sector. The programs are unique to the FHLBank System. The FHLBanks’ Affordable Housing Program and voluntary initiatives are made possible by their unique public-private structure, the strength and diversity of their nationwide membership, the success of their liquidity mission, and the enduring relationships they’ve built with thousands of members and partner institutions across all 50 states and four U.S. territories.

Local Knowledge, National Reach

The R Street article also incorrectly characterizes the FHLBanks as rent-sharing vehicles for insiders. This could not be further from the truth. FHLBanks are open and available to any eligible member and serve approximately 6,500 institutions large and small, urban and rural. The cooperative model enables regional responsiveness and ensures that community-focused lenders—those most attuned to local housing needs—have access to reliable liquidity and affordable housing support. As discussed in a recent article, the FHLBanks’ deep membership base combines the resources of larger members with the local expertise of smaller, community members. This is a modern-day application of the Pareto principle: the actions of a few empower and enable the many.

As the FHLBanks’ 2024 Impact Report notes, the FHLBanks finished the year with over $1 trillion of liquidity products supporting members and the U.S. financial system. The stability this provides to small lenders cannot be overstated—nor can its downstream benefits to households, local governments, builders, and job creators.

Support for Improvements Grounded in Reality

Constructive ideas for strengthening the FHLBanks are always welcome, and the System remains committed to ongoing improvement. But recommendations must be based on fact, not ideology. Ignoring the reality that the FHLBanks are vital partners to their members and to the communities served by those members means ignoring their integral role in a healthy, functioning housing and financial system.

The truth is simple: the Federal Home Loan Banks are not part of the problem—they are a critical part of the solution. They exist not to create risk, but to manage and contain it. Not to distort markets, but to support them. Not to enrich insiders, but to empower communities.