The national housing shortage is one of the great intractable problems facing the country. Politicians from both parties, economists, executives, policymakers, and regulators are focused on a range of issues to be resolved: zoning, regulation, supply‑demand imbalances, demographics, financing costs, taxes, insurance, and labor constraints. A coordinated, multi-pronged response across federal, state, and local stakeholders is required to tackle these issues and the FHLBanks are advancing solutions to help address housing affordability and supply.

A recent opinion piece in the New York Times[1] argues that the FHLBanks should be restructured to focus on multifamily construction lending as a cure-all for housing affordability. This proposition rests on the flawed premise that FHLBank liquidity is not delivering for housing finance and instead is “specialized” in providing cheap funding to large financial institutions, revealing a fundamental misunderstanding of both U.S. housing challenges and the realities of FHLBank operations, mission, and membership.

The System has roughly 6,400 members including community banks, credit unions, insurance companies, and CDFIs and provides liquidity to thousands of members daily.[2] This stands in direct contradiction to the claim that the FHLBanks serve only large lenders, a claim that ignores the breadth of member participation and the fact that broad-based membership is a defining feature of the FHLBanks’ cooperative model.[3]

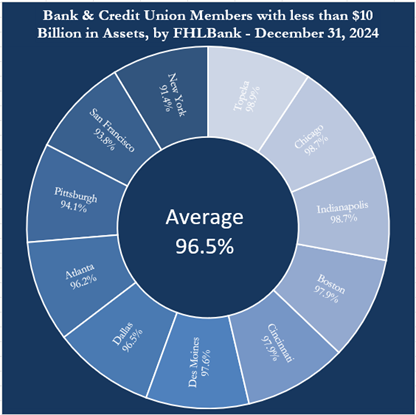

Community-based lenders have always been at the heart of the System. As shown in Figure 1, small community bank and credit union lenders with less than $10 billion in assets represent an overwhelming 96.5 percent of FHLBank depository members, underscoring the System’s support for local lending and local economies nationwide. While regulatory changes over the past two decades have driven a major shift in mortgage origination from depositories to nonbanks, a recent report found that 98% of depository institutions engaged in mortgage origination are members of the FHLBank System.[4]

Figure 1: FHLBank Membership Primarily Small Depository Lenders

Likewise, the assertion that the FHLBanks are not fulfilling their mission reflects a clear misunderstanding of what that mission is. Though Congress has refined the FHLBanks’ operations and membership over time to meet changing market needs, the core mission has remained the same for nearly 100 years – to provide stable, reliable liquidity to members to support housing and community investment. This point is worth repeating. Everything the FHLBanks do – whether it is providing advances (loans), purchasing mortgages, issuing letters of credit, or distributing grants for affordable housing – they do through their members, the financial institutions that directly serve consumers and small businesses every day. Moreover, the FHLBanks only engage in activities that Congress has determined for them, pursuant to their mission. Otherwise stated, all FHLBank activity is mission activity.

Research by the Urban Institute demonstrates that FHLBank advances lead to significant increases in lending by bank and credit union members with even greater impacts at smaller financial institutions.[5] The Urban Institute found that increases in FHLBank advances increased lending by over $1.8 trillion, with significant increases in real estate lending and mortgage originations. In a separate analysis by the Urban Institute, the FHLBanks’ liquidity was found to provide economic stabilization benefits to the U.S. economy to the tune of $21.4 billion annually, 3.1 times greater than the $6.9 billion annual benefit the Congressional Budget Office estimated the FHLBanks receive from their government-sponsored enterprise (GSE) status.[6]

A 2025 report by the Government Accountability Office (GAO) found the FHLBanks “serve as a reliable and consistent source of funding for banks of all sizes throughout the financial cycle.” GAO’s analysis underscores how the liquidity the FHLBanks provide strengthens the resilience of local financial institutions, increases homeownership and small business lending, and promotes overall financial stability.[7]

What’s more, recent survey evidence from the American Bankers Association, shows that FHLBank liquidity supports lending across single-family residential homes, multifamily apartment homes, small business, and community investment, providing liquidity where financing gaps persist.[8]

Taken together, the evidence from Urban Institute, GAO, ABA, and others demonstrates that the FHLBanks are fulfilling their mission by providing stable, collateralized liquidity to members, which in turn expands homeownership lending, small business activity, and broader community investment, precisely as Congress intended.

The notion that repurposing the FHLBank System into a direct lender for multifamily housing construction is a “no-cost” solution is both false and potentially harmful to communities and our broader economy. For nearly a century, the FHLBanks have provided reliable liquidity to members and supported the nation’s housing finance system – and supported economic revitalization. Disrupting a model that has functioned effectively for so long would be imprudent and would risk credit availability, financial stability, and economic growth. Ideas that sound good in an opinion piece must survive in the light of rational scrutiny.

The FHLBank System already supports the full spectrum of housing finance with liquidity flowing to large multifamily developments, smaller “missing middle” 5- to 49-unit developments, and single-family homes. As shown in the 2024 Impact Report, the FHLBanks supported construction of more than 51,000 units of housing and helped more than 68,000 families with homeownership in 2024.[9] In addition, as reported in their 2025 Combined Financial Report, the FHLBanks help recirculate housing liquidity with more than two-thirds of single-family mortgages held by portfolio lenders pledged as collateral.[10] Forcing a shift away from the FHLBanks’ core liquidity function into higher-risk, development stage construction lending would not be a no-cost additive solution; it would be a substitution with real opportunity costs, including reduced liquidity and stability for members during periods of market stress.

By forcing concentration of FHLBank liquidity into an activity that carries significantly more credit risk, execution risk, and market risk, the countercyclical capacity of the FHLBanks would be weakened, exposure to localized real estate downturns would increase, and overall financial stability could be jeopardized.

The argument that only 10 percent of FHLBank net income goes to the System’s intended mission not only reflects a misunderstanding of that mission, but it also discounts the broader impact of its affordable housing and community development activities.

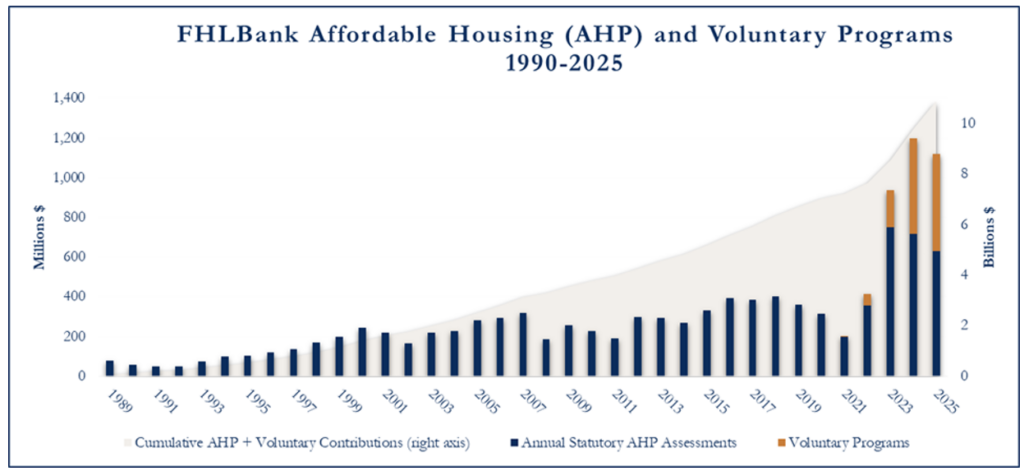

The FHLBanks contributed more than $1 billion in both 2024 and 2025 to affordable housing and community investment through statutory and voluntary programs. Critiques of the System often focus solely on statutory Affordable Housing Program (AHP) assessments, overlooking the positive impacts of the FHLBanks’ fulfillment of their liquidity mission and overlooking the dozens of voluntary programs the FHLBanks have set up in recent years. The FHLBanks’ contributed more than $1 billion to voluntary AHP and other voluntary programs in just the past two years alone.[11] The significant increase in AHP and voluntary program funding in recent years is clear in Figure 2. Beyond grants, the System supports housing at scale with a mortgage portfolio of nearly $80 billion and targeted advance programs, including CICA and CIP, which provide discounted funding for housing and community investment.[12]

Figure 2: FHLBank Expansion of Affordable Housing Program and Voluntary Programs

The suggestion that the FHLBanks target assistance to households at or below 80 percent of area median income overlooks the fact that FHLBank programs already focus on this socioeconomic group. AHP set-aside and competitive grants serve these low- and moderate-income households. In programs where FHFA has set goal thresholds, in most, if not all, cases the FHLBanks have exceeded the thresholds, with far greater levels of support reaching the targeted populations.[13]

The FHLBank System is not a relic in need of reinvention. It has remained true to its mission for nearly a century, evolving to meet changing needs while continuing to provide stability and reliable liquidity that supports housing finance and community investment through member institutions nationwide. The challenge is not to repurpose the System, but to recognize and build upon the daily collateralized liquidity the FHLBanks deliver, as Congress intended, to the community lenders that anchor Main Street, helping renters, homeowners, and local economies thrive.

[1] Opinion | This Is Why America Is Short Four Million Homes – The New York Times

[2] In 1932, the FHLBanks were established to provide liquidity to insurance companies and thrifts (originators and investors in mortgages). Over time, Congress expanded membership eligibility to include credit unions and community development financial institutions (CDFIs).

[3] Policy Brief: Prudent Management Enables FHLBank Support for Members and Communities – FHLBanks

[4] https://www.urban.org/sites/default/files/2026-01/Final_The_Value_of_the_FHLBank_System_to_Promote_Lending_0.pdf

[5] The Value of the FHLBank System to Promote Housing and Community Development Lending | Urban Institute

[6] The Value of the FHLBank System to Bank Liquidity and Stability | Urban Institute

[7] Federal Home Loan Banks: Role During Financial Stress and Members’ Borrowing Trends and Outcomes | U.S. GAO

[8] Policy Brief: ABA Survey Shows FHLBanks are Critical Partners in Community Bank Liquidity and Stability – FHLBanks

[9] 2024 Impact Report | FHLBanks

[10] For the FHLBanks, Collateral is Foundational – FHLBanks

[11] https://www.fhlb-of.com/ofweb_userWeb/resources/2025Q4CFR.pdf

[12] https://www.fhlb-of.com/ofweb_userWeb/resources/2025Q4CFR.pdf

[13] 2024 Impact Report | FHLBanks