Key Takeaways from the CSBS 2024 Annual Survey of Community Banks

This month the Conference of State Bank Supervisors’ (CSBS) released results of their 2024 Annual Survey of Community Banks. The survey reflects responses by 370 community bank respondents from 38 states. Top concerns of respondents were cybersecurity, regulatory burden, technology costs, and cost of funds.

Funding costs and regulation were nearly tied in the 2024 rankings for the most important external risk. Net interest margins and core deposit growth also ranked highly among surveyed banks, a theme also present in the 2023 survey and consistent with the high-interest rate environment. The jump in regulation to nearly the top spot reflects growing concern about the impacts of regulatory burden and overreach among community bankers over the last few years.

The survey also found that attracting and retaining core funding has been increasingly difficult for community banks. Fortunately, community banks that are Federal Home Loan Bank (FHLBank) members can rely upon their FHLBank to provide reliable, everyday liquidity to support lending, assetliability management, and funding for affordable housing and community development.

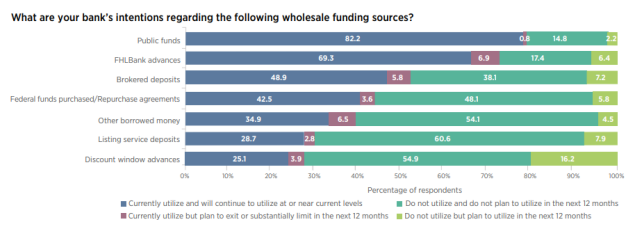

The survey found that 69.3 percent of community bank respondents currently utilize FHLBank advances (loans) and intend to continue doing so, while 6.4 percent said they do not currently utilize FHLBank advances but plan to rely upon their FHLBank for liquidity to support lending and operations in the coming 12 months.

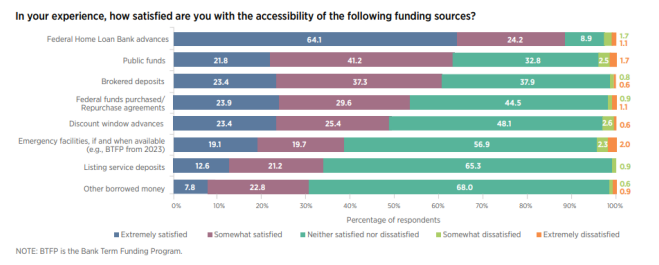

In addition, the FHLBanks were found, by a large margin, to deliver funding with the greatest ease of use (accessibility) of any funding source. The CSBS survey found 64.1 percent of respondents were “Extremely satisfied” with FHLBank advance accessibility, nearly three times the next highest rated source of funding, Fed Funds purchased/Repurchase agreements, which had a 23.9 percent “Extremely satisfied” accessibility rating.

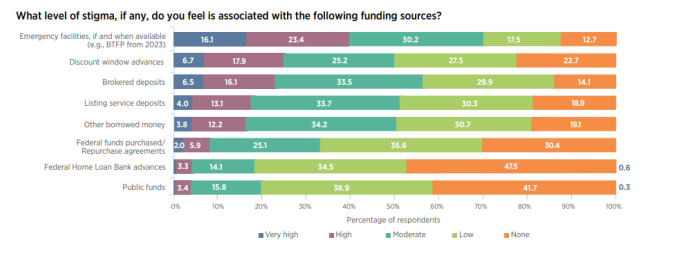

The survey also asked respondents about the stigma associated with various funding sources. FHLBank advances and public funds were reported as having the lowest level of stigma. FHLBank advances were reported as having the lowest stigma with 82.0 percent of respondents reporting “None” or “Low” stigma associated. Conversely, the Federal Reserve discount window and emergency funding (such as Bank Term Funding Program “BTFP”) were reported by 50.0 percent and 30.2 percent of respondents as having “None” or “Low” stigma.

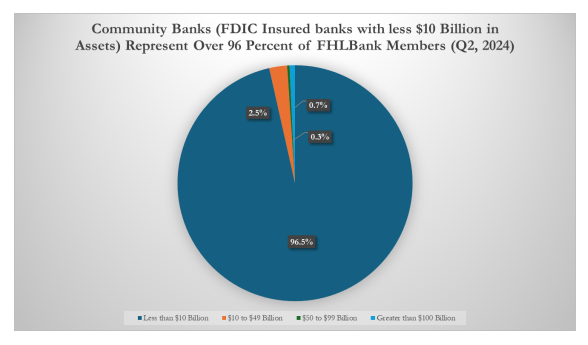

The result of the 2024 CSBS Annual Survey of Community Banks demonstrates the strong connection between the FHLBanks and community bankers across the country. Moody’s Analytics reported that small bankers have the highest ratio of loans to deposits, putting more capital to work for their communities (see October 2024 Facts You Can Bank On). With Community Banks accounting for over 96 percent of FDIC insured FHLBank members, the FHLBanks are proud of the affordable housing and community development efforts supported by our community banker members in communities across the country.