In an environment marked by economic uncertainty and market volatility, the Federal Home Loan Bank System continues to do what it was designed to do: provide reliable, countercyclical, real estate-collateralized liquidity that strengthens financial institutions, increases lending, and supports communities across the country.

The evidence is clear—and increasingly hard to ignore.

- A November 2025 report from the Urban Institute estimated that the FHLBanks generate up to $21.4 billion annually in economic stability benefits to the U.S. economy.[1]

- A December 2025 report from the U.S. Government Accountability Office (GAO) found that the FHLBanks “generally serve as a reliable and consistent source of funding throughout the financial cycle,” “play a key role in the health of small banks,” and that higher borrowing from the FHLBanks is associated with increased real estate lending, lower risk of being flagged as a problem bank, and lower probability of failure or voluntary closure.[2]

- A January 2026 Urban Institute analysis found that increases in FHLBank advances contributed to $1.82 trillion in additional lending by member banks and credit unions, with the greatest impacts among smaller institutions and in the post-2008 period.[3]

- A May 2026 Urban Institute study found that the FHLBanks deployed more than $147 billion for housing and community development programs from 2015-2024, generating over $47 billion in economic impact, while consistently exceeding statutory Affordable Housing Program targets.[4]

In short, the FHLBanks are working exactly as intended — delivering real, measurable benefits to financial institutions, communities, and the broader economy.

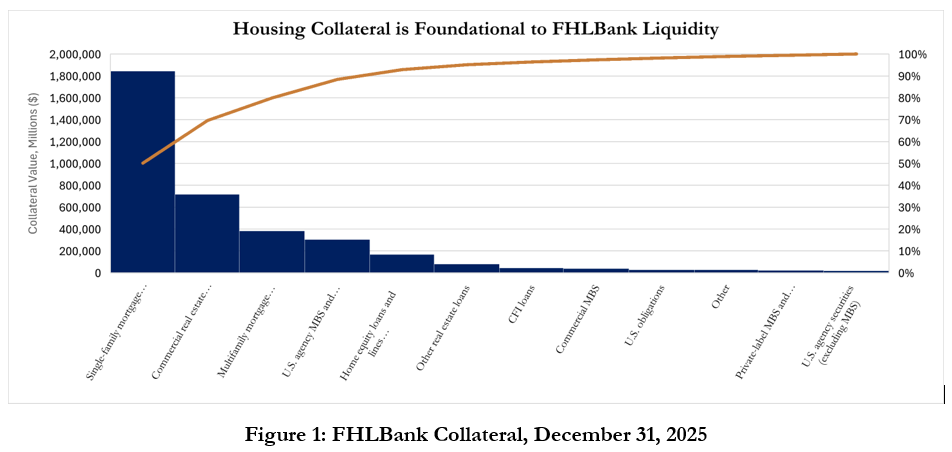

Despite this growing body of empirical evidence, an April 2026 paper by Aaron Klein and Chris Hughes treats the FHLBank System’s role as a reliable liquidity provider as peripheral to their mission.[5] In their framing, the FHLBank System was created primarily to “support homeownership.” While the FHLBanks do support homeownership, that characterization is an incomplete oversimplification. The FHLBanks were established to provide liquidity, backed by eligible collateral (see Figure 1), to lending institutions to support housing finance – a mandate rooted as much in market stability and funding capacity as in housing outcomes.

Elsewhere, Klein and Hughes argue that the purpose of the FHLBanks is to “finance housing at scale.” But providing liquidity to housing lenders is precisely the mechanism Congress chose to achieve that objective. The FHLBanks were not created to originate mortgages, construct homes, or directly subsidize housing production. They were created to ensure that financial institutions had reliable access to funding so that housing credit could continue to flow through all market conditions. Liquidity is not separate from the mission; it is how the mission is carried out.

That distinction is important. Overlooking the FHLBanks’ core liquidity function leads to an overly narrow interpretation of mission activity – one that only treats activities that directly fund housing as aligned with the System’s core mission. This is inconsistent and at odds with the origin story of the FHLBanks and their raison d’etre.

Indeed, assertions that the FHLBanks have somehow strayed from their mission often rest on an unduly narrow understanding of what that mission is. The mission of the FHLBank System is not self-defined; it is established by Congress. Since 1932, Congress has affirmed and reaffirmed the System’s core role as a provider of liquidity to member institutions, reflecting the longstanding view that stable and reliable funding is essential to a well-functioning housing finance system.

Despite acknowledging that “financing costs are the most volatile constraint” on multifamily construction, Klein and Hughes treat the need for liquidity (i.e., the need for funds to finance housing) as a separate matter from housing construction.

Klein and Hughes also claim “[t]he United States spends about $6.9 billion annually in implicit federal subsidies” on a system “that no longer serves its housing mission.”

This is wrong on multiple levels.

First, the United States spends $0 annually on the FHLBank System. The System is privately owned, member-capitalized, and operates wholly without federal appropriations. The CBO report the authors reference in their paper clearly acknowledges that “Congress does not appropriate funds for [the Home Loan banks].”[6]

Second, the assertion that the FHLBank System no longer serves its mission is contradicted not only by the Urban Institute and GAO findings cited above, but also by reporting from the System’s regulator, the Federal Housing Finance Agency, and by the FHLBanks’ publicly reported data. Yet, Klein and Hughes do not recognize this growing body of evidence.[7]

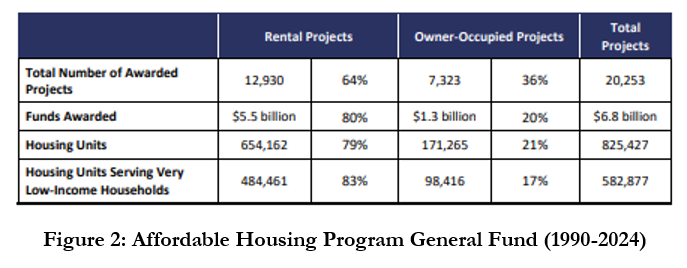

Figure 2 – from FHFA’s October 2025 Targeted Mission Report – shows that the FHLBanks’ Affordable Housing Program General Fund supported more than 825,000 affordable housing units, with more than one-third serving rural areas and more than 70% of units benefiting very low-income households.[8]

Instead of doubling down on a structure that has worked for 94 years, Klein and Hughes propose a radical transformation of the FHLBanks from wholesale liquidity providers into direct construction lenders that allocate 25% of advances—roughly $175 billion—to construction lending. Far from a modest proposal, this represents a fundamental redesign of a system that members and communities have relied upon for decades. It would harm community banks, weaken U.S. financial stability, increase risk to the broader U.S. economy, and push the Federal Home Loan Bank System away from its core mission in the following ways:

- It moves the FHLBanks away from their Congressional mission

For nearly 100 years, the FHLBanks have operated as collateralized liquidity providers to member institutions, not as direct lenders. This structure ensures that credit decisions remain with institutions that have local knowledge, underwriting expertise, and borrower relationships.

Converting the Federal Home Loan Banks into direct lenders would abandon this model, replacing a proven system with one Congress never authorized.

- It dramatically increases risk

The FHLBanks were built to provide stability as low-risk, overcollateralized liquidity providers. Transitioning to construction lending—historically one of the riskiest asset classes—would fundamentally alter that profile. Scenario analysis indicates the change could result in:

- Losses of $8 billion in a moderate downturn, and

- Up to $16–$22 billion in a severe stress scenario based on a 2021 FDIC analysis.[9]

At the same time, accounting rules would require billions of dollars in reserves, placing a strain on capital that could increase funding costs for the FHLBanks and their members. Even modest spread widening would add billions in annual interest expenses, eroding the funding advantage that allows FHLBanks to support members and communities nationwide.

- It creates “wrong-way risk”

The most serious flaw is structural. The same conditions that produce construction loan losses—rising rates, declining property values, tightening credit—are precisely when members need liquidity the most. Under the Klein/Hughes proposal, the FHLBanks would face the triple-whammy of rising credit losses, rising member demand for liquidity, and rising funding costs all at the same time! That is not diversification or smart policy, it is concentration of risk at the worst possible moment.

- It turns the FHLBanks from reliable partners into competitors with their own members

Each FHLBank is a member-owned cooperative and each is owned and capitalized by their members—community banks, credit unions, insurance companies, and CDFIs – the very institutions that originate construction loans today.

Under the proposal, the FHLBanks would:

- Compete directly with members for staff,

- Compete directly with members for loans,

- Undercut members with below-market pricing, and

- Draw in riskier borrowers through adverse selection.

This would undermine the cooperative model that Congress authorized nearly 100 years ago and weaken the institutions the FHLBank System was created to support.

- It is operationally unrealistic

The FHLBanks do not currently originate construction loans and for good reason. Doing so at scale would require specialized staff for underwriting, monitoring, and servicing, along with the appropriate systems and nationwide developer relationships. Building this capacity would require a huge investment in people, systems, and capacity, potentially surpassing the size of the current FHLBank workforce. And where would this capacity come from? One likely source would be FHLBank members that have staff with the relevant on-the-ground knowledge and relationships for this type of lending. Thus, the FHLBanks would be competing directly with their members for talent, weakening both the institutions that System was designed to support and the cooperative foundation that gives the System its strength.

If the goal is to increase FHLBank support for housing supply and community investment, the answer is not to pull the FHLBank System away from its liquidity mandate and create new competition for its members. Instead, the approach should be to leverage the knowledge and relationships the Federal Home Loan Bank System has built over nearly 100 years to meet the current moment.

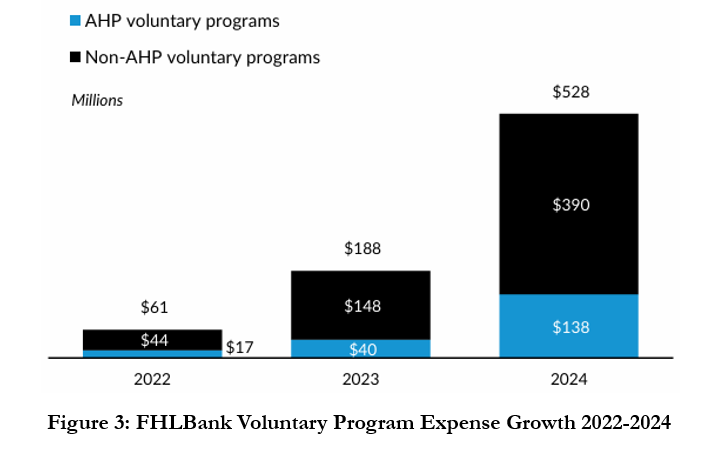

Across the 11 FHLBanks, the System has responded to member and district needs with reliable liquidity across the economic cycle, by fulfilling and exceeding its statutory AHP requirements, and by developing new voluntary programs, scaling existing initiatives, and delivering targeted solutions tailored to local markets. As reported by the Urban Institute, the FHLBanks more than tripled voluntary contributions for housing and community investment programs in 2023 and in 2024 the System more than doubled voluntary contributions again, in addition to the support provided through AHP and other programs. These are not theoretical ideas, these are active programs, documented in the FHLBanks’ Impact Reports and Combined Financial Reports and already producing results.[10]

From 2023 to 2025, the FHLBanks averaged over $1 billion annually in combined AHP assessments and voluntary housing and community investment contributions. That momentum has continued—and accelerated—into 2026, where we see Q1 2026 statutory AHP plus voluntary contributions at a record level, higher than any first quarter in system history. This is what responsiveness looks like in practice: a System that listens to its members, adapts to local needs, and delivers capital where it is most effective—through, not around, the institutions that know their communities best.

The strength of the FHLBanks is not in going around their members as Klein and Hughes suggest, it is in supporting and strengthening them. The number of FDIC insured banks in the United States over the past 25 years has declined from over 10,000 to less than 4,300 today. The remaining depository lenders need strong, reliable partners, not new competition.[11] The FHLBanks derive their strength from their members and the relationships that have enabled the System, for nearly a century, to provide liquidity, stability, and investment when and where it is needed most.

Now is not the time to replace the FHLBanks’ proven, low-risk cooperative model with a new, riskier, direct lending approach that undermines the very institutions that power housing and community development on the ground. After nearly 100 years, the Federal Home Loan Bank System is delivering every day—for its members, for communities, and for the U.S. economy. The lesson is simple and enduring: collateralized, member-driven liquidity isn’t a flaw, it is the mission and it works for members and for America.

[1] https://www.urban.org/research/publication/value-fhlbank-system-bank-liquidity-and-stability

[2] https://www.gao.gov/assets/gao-26-107373.pdf

[3] https://www.urban.org/research/publication/value-fhlbank-system-promote-housing-and-community-development-lending

[4] https://www.urban.org/research/publication/value-fhlbank-systems-housing-and-community-mission-oriented-programs

[5] https://www.brookings.edu/articles/reform-the-federal-home-loan-banks-to-finance-the-housing-america-needs/

[6] https://www.cbo.gov/system/files/2024-03/59712-FHLB.pdf

[7] https://www.fhfa.gov/document/d/fhlb-tmr/2024-federal-home-loan-bank-targeted-mission-report; https://fhlbanks.com/2025-impact-report/; https://fhlbanks.com/impact-report/

[8] https://www.fhfa.gov/document/d/fhlb-tmr/2024-federal-home-loan-bank-targeted-mission-report

[9] https://www.fdic.gov/analysis/cfr/working-papers/2021/cfr-wp2021-07.pdf

[10] https://www.fhfa.gov/document/d/fhlb-tmr/2024-federal-home-loan-bank-targeted-mission-report; https://fhlbanks.com/2025-impact-report/; https://www.fhlb-of.com/ofweb_userWeb/resources/2026Q1CFR.pdf; https://www.urban.org/sites/default/files/2026-05/Final_The_Value_of_the_FHLBank_Systems_Housing_and_Community_Mission_Oriented_Programs_0.pdf