The Congressionally chartered Federal Home Loan Banks provide liquidity and other services to strengthen and stabilize thousands of financial institution members in all 50 states, the District of Columbia, and three U.S. territories. The FHLBank System consists of 11 privately capitalized, member-owned cooperative banks, regionally situated across the country, serving approximately 6,500 commercial banks, credit unions, savings institutions, insurance companies, and community development financial institutions (CDFIs).

In our capitalist economic system individuals and companies are rewarded for their investment of private capital to grow the economy. When investments are made wisely and market conditions align, the attending rewards are earnings and capital appreciation. When private capital is not invested wisely or market conditions turn against a company or industry, investors may lose their investments and companies may shutdown.

According to Forbes, over the 10-year period from 2014-2023, there were an average of 5.2 bank failures each year. In March 2023, a digital run on a handful of regional banks resulted in deposit flight from the banking system at a historically rapid rate. The FHLBank System responded with the largest single-week funding of advances in its history, providing stability for members and the broader financial system. Despite these efforts, four member banks failed between January and May of 2023. The four failed banks represented 0.06 percent of FHLBank System membership.

By the end of the first quarter, normal operations had returned to the financial markets and approximately 56% of FHLBank members were using FHLBank advances for liquidity to serve their customers and strengthen their balance sheets. The remaining 44% of FHLBank members did not have outstanding advances at the end of the quarter but continued to serve their customers with confidence that if needed, they could turn to their FHLBank for liquidity to support them and their customers.

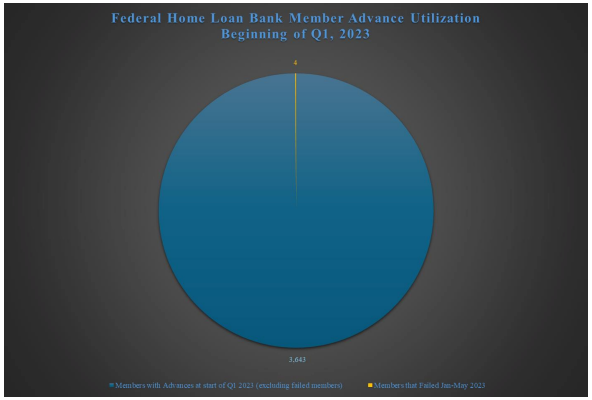

The pie chart below shows FHLBank members with advances at the beginning of the first quarter of 2023. The four banks that failed are highlighted in gold at the top of the figure (may have to zoom in). The failed banks represented only 0.1 percent of members with outstanding advances at the start of the year. The remaining 99.9% of members that used FHLBank advances for liquidity weathered the storm and continued to serve their homebuyer, small business, and commercial customers. Clearly, any assertion that FHLBank liquidity is used only, or primarily, as support for troubled institutions is not supported by the data. Rather, the data show that the vast majority of FHLBank members rely on advances for funds throughout the year – including during times of stress. This dependable source of liquidity makes the housing finance sector and the U.S. economy stronger and more resilient.