Housing policy has received renewed bipartisan attention in Congress as communities seek to improve affordability and address housing supply shortages across the country. This has prompted some to reconsider the Federal Home Loan Bank (FHLBank) System and whether the FHLBanks’ model of providing reliable, on-demand liquidity to members is the appropriate framework for supporting affordable housing. This policy brief reviews the available data and shows that the FHLBanks’ are indeed delivering on their liquidity mission to support members, communities, housing supply, and the U.S. system of housing finance.

Background

A fundamental point that is often overlooked in policy discussions is the centrality of the FHLBanks’ liquidity function. As established by Congress, the FHLBanks’ core mission is to provide liquidity to members to support housing finance and community development through all economic cycles. The System’s affordable housing and community investment programs are made possible through the successful execution of this core function – providing reliable liquidity is the foundation.

Congress created the FHLBank System in 1932 to serve as a stable source of liquidity for member financial institutions through changing economic conditions. The System fulfills this mission primarily through advances – fully collateralized loans provided by the FHLBanks to member institutions. Advances are customizable to meet members’ funding needs, with terms ranging from overnight up to 30 years, fixed or variable interest rates, along with other customization to meet members’ needs. The significance of this liquidity function is straightforward but cannot be understated.

Traditionally, depository institutions accepted deposits and made loans with those funds to meet local lending demand. The depository lending model works as long as deposits are sufficient to meet demand. However, once deposits are fully extended into loans, lending capacity is restricted until additional funding becomes available. This constraint can delay or prevent otherwise creditworthy projects from being financed, hindering economic growth and opportunity. The FHLBanks were created to solve this liquidity constraint by providing members with a dependable source of funding across all market conditions.

Funding When and Where it is Needed

If a prospective home buyer needs a mortgage for a home, a small business needs financing to expand, or a local government needs funding for an infrastructure project, FHLBank members can respond and meet those needs even if deposits are scarce. FHLBank members can pledge eligible collateral to their FHLBank to secure the funding needed to meet the demands in their communities.

In this way, the FHLBanks help ensure that credit continues to flow to households, businesses, and communities. The liquidity they provide to members, primarily through advances (loans), is much more than a simple balance-sheet tool, it is an integral part of the financial infrastructure that enables members to continue lending through changing economic conditions.

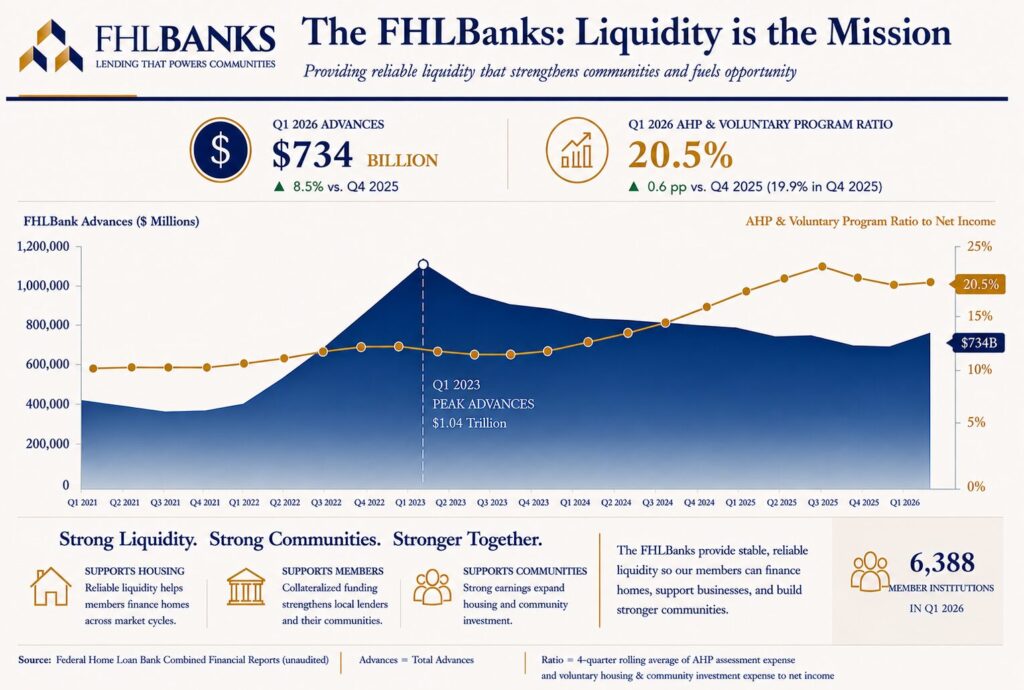

The FHLBanks deliver on their core liquidity mission every day, as demonstrated in Figure 1. After reaching a cyclical low in 2021, advances increased in 2022 and have remained at around $800 billion for 15 consecutive quarters, demonstrating the sustained demand for and value of FHLBank liquidity. At the end of the first quarter of 2026, outstanding advances to member commercial banks, savings institutions, credit unions, insurance companies, and community development financial institutions (CDFIs) were more than double their 2021 lows. This sustained level of support underscores the crucial role of the FHLBank System and shows that it is operating as designed – delivering liquidity to members when and where it is needed most.[1]

Figure 1 – FHLBank Mission Achievement

The Core Liquidity Mission Makes Support for Housing Possible

Successful execution of the FHLBanks’ core liquidity function generates earnings and strengthens the cooperative model, returning value back to members and communities through multiple channels. As member-owned cooperatives, the FHLBanks deliver value through:

- Reliable, on-demand collateralized funding;

- Affordable housing and community investment programs;

- Dividends to member institutions; and

- Retained earnings that build capital and strengthen the capacity to serve members.

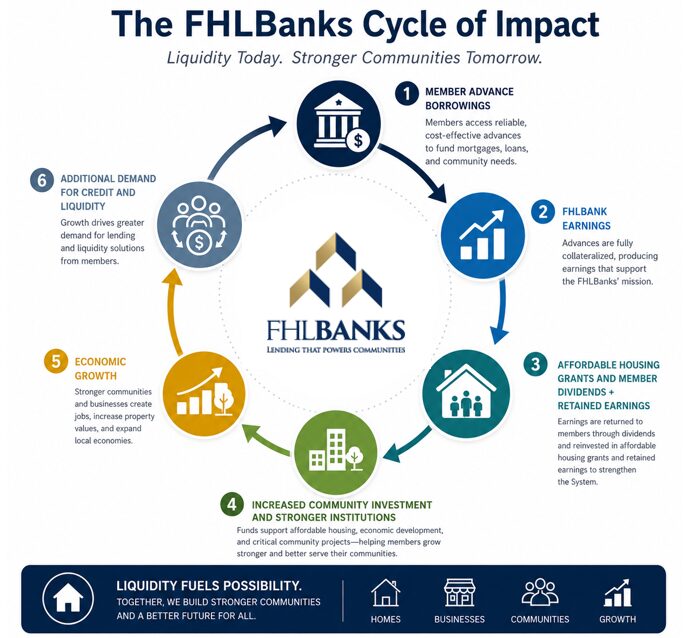

As illustrated in Figure 2, fulfillment of the FHLBanks’ liquidity mission generates a virtuous cycle that has enabled the System to support members and communities for 94 years at no cost to taxpayers, while remaining safe, sound, and fully self-capitalized.

Figure 2 –FHLBank Liquidity Strengthens Members and Communities

Figure 2 –FHLBank Liquidity Strengthens Members and Communities

The FHLBanks’ ability to support housing finance and community development begins with the System’s core liquidity function. Collateralized advances provide members with reliable funding to meet customer and community lending demands. Earnings generated from the FHLBanks’ liquidity programs support affordable housing and community investment grants, which help expand homeownership opportunities and strengthen local economies. Dividends on member capital stock provide income to members, strengthen member capital positions, and increase member lending capacity. While retained earnings build the FHLBanks’ capital base and ensure the System remains safe and sound, preserving the capacity to meet the current and future demands of their cooperative members.

Affordable Housing Program History

Though the FHLBanks have existed since 1932, Congress did not establish the Affordable Housing Program (AHP) until 1989, as part of the Financial Institutions Reform, Recovery, and Enforcement Act (FIRREA) of 1989.[2] Affordable housing programs are a key component of the FHLBanks’ public mission and are made possible by successful fulfillment of their core liquidity function. Under FIRREA, each FHLBank is required to contribute a portion of each year’s earnings toward the AHP. Initially, the requirement was set at five percent, rising to 10 percent beginning in 1995.

Mission Achievement and Mission Alignment

Critics sometimes assert that the FHLBanks “only” contribute 10 percent of earnings to affordable housing. This criticism indicates a misunderstanding of the FHLBanks’ mission, Congressional intent, and actual FHLBank programs. As noted above, the affordable housing program statute states that each FHLBank is to contribute “10 percent of the preceding year’s net income, or such prorated sums as may be required to assure that the aggregate contribution of the Banks shall not be less than $100,000,000 for each such year.”[3] In 2025, the FHLBanks contributed $632,000,000 to their affordable housing programs, more than six times the annual minimum amount.

As reported in FHFA’s Annual Report to Congress, the FHLBanks’ Combined Financial Reports, and the FHLBanks 2025 Impact Report, the FHLBanks are performing precisely as Congress directed.[4},[5],[6] Each of the 11 FHLBanks meets its statutory AHP requirements. Significantly, the costs incurred to administer and operate this statutory program are borne by the individual FHLBanks and not deducted from the 10 percent annual assessment. The end result is that 100 percent of AHP assessments are awarded to support affordable rental housing and affordable homeownership initiatives.

But the story does not end with the statutory requirement. In recent years, the FHLBanks have substantially expanded housing and community investment above and beyond the Congressional requirement (Figure 1).

The FHLBanks have:

- Increased voluntary contributions to supplement AHP funding;

- Expanded homeownership assistance programs;

- Created additional voluntary housing and economic development initiatives;

- Developed targeted programs to address local and regional needs; and

- Increased support for underserved populations and communities.

The FHLBanks’ 2025 Impact Report, released in May 2026, listed approximately 60 voluntary programs that the FHLBanks created and are operating to address unique district needs based on consultations with FHLBank members, Affordable Housing Advisory Councils (AHAC), and Boards of Directors.[7]

Voluntary programs support:

- Affordable rental housing production and preservation;

- Homeownership opportunities;

- Senior housing;

- Veteran housing;

- Middle-income housing;

- Tribal housing and investments on Tribal lands;

- Disaster recovery and resilience initiatives;

- Jobs programs; and

- Broader community and economic development activities.

Figure 1 shows that statutory AHP assessments plus voluntary contributions averaged more than 15 percent of net income on a rolling four-quarter basis from Q1 2021 through Q1 2026 and have exceeded 20 percent, on average, over the most recent six quarters. In other words, critics who focus solely on the statutory 10 percent requirement are missing the forest for the trees – the FHLBanks’ total housing and community investment contributions have doubled the statutorily required amount in recent periods!

Moreover, since AHP contributions are statutorily set as a percentage of earnings, as advances and earnings grow, funding for housing and community investment increases commensurately. Figure 1 shows that advances more than doubled from their 2021 lows, and at the same time, the FHLBanks expanded voluntary initiatives, delivering a dramatic increase in housing and community investment funding. In 2025, the combined dollar value of statutory AHP assessments and voluntary contributions was over $1.1 billion, more than five times the amount delivered in 2021. This is both mission alignment and mission achievement.

Few institutions have responded as rapidly and meaningfully to rising community needs as the FHLBanks. The FHLBank System represents a uniquely American institution. Member institutions capitalize the FHLBanks, which, in turn, provide liquidity that enables members to better serve customers and communities. Earnings generated from FHLBank member activities support affordable housing and community investment, provide dividends to members, and build retained earnings that strengthen the cooperative.

Liquidity is therefore not separate from affordable housing—it is the foundation upon which the FHLBanks’ housing and community investment programs are built. As noted in a March article, the FHLBanks’ support for housing has always been linked to the liquidity mission through collateral, based on collateral eligibility set by Congress.[8] The success of the FHLBanks’ liquidity programs ensures the success of the FHLBanks’ community support programs and conversely, policies or actions that hinder the successful execution of the FHLBanks’ liquidity programs, necessarily reduce support for AHP, voluntary initiatives, and community investment. For over nine decades, the FHLBanks have executed on their Congressionally established mission to support members and communities across the U.S.

As America celebrates its 250th anniversary, the FHLBanks remain true to the mission Congress established nearly a century ago: delivering liquidity that keeps credit flowing, communities growing, and families knowing that the American dream remains within reach in communities across the country.

[1] https://www.fhlb-of.com/ofweb_userWeb/resources/2026Q1CFR.pdf

[2] https://www.govinfo.gov/content/pkg/STATUTE-103/pdf/STATUTE-103-Pg183.pdf

[3] https://www.govinfo.gov/content/pkg/USCODE-2020-title12/pdf/USCODE-2020-title12-chap11.pdf

[4] https://www.fhfa.gov/document/d/arc/fhfa-2025-annual-report-to-congress.pdf

[5] https://www.fhlb-of.com/ofweb_userWeb/resources/2026Q1CFR.pdf

[6] https://fhlbanks.com/2025-impact-report/

[7] https://fhlbanks.com/2025-impact-report/

[8] https://fhlbanks.com/for-the-fhlbanks-collateral-is-foundational/