For 94 years, the Federal Home Loan Banks (FHLBanks) have provided reliable liquidity to help their members finance homes, support affordable housing, strengthen communities, and promote economic growth. Because the FHLBanks fulfill this mission through a diverse membership and a wide range of housing finance activities, no single dataset fully captures the housing finance support provided by the FHLBank System.

However, critics of the System sometimes point to Home Mortgage Disclosure Act (HMDA) data to argue that members that do not appear in the HMDA data are not supporting or aligned with the System’s housing finance mission. For example, a 2023 article published by Bloomberg asserted that 42 percent of FHLBank members had not reported making a single mortgage over the previous five years.[1] The authors of the article relied on HMDA to support that conclusion.

The problem with this type of analysis is that it treats HMDA as a complete measure of mortgage lending activity and draws conclusions that the data was never intended to support. Doing so misrepresents both the purpose of HMDA and the role of FHLBank members in the housing finance ecosystem. HMDA is a targeted regulatory reporting database tool designed to promote transparency and support fair lending oversight, but it does not represent a complete picture of all mortgage activity.

Congress enacted the Home Mortgage Disclosure Act in 1975 to improve mortgage market transparency, help determine if financial institutions were serving the housing needs of their communities, assist public officials in directing public-sector investment, and identify potential discriminatory lending patterns for enforcement of fair lending laws. HMDA was not designed to capture every mortgage transaction or every institution engaged in housing finance. Rather, as implemented through the Consumer Financial Protection Bureau’s Regulation C, HMDA establishes reporting requirements for certain financial institutions – primarily depository institutions and non-depository mortgage lenders – that meet specified coverage requirements and loan volume thresholds. As a result, HMDA captures a significant portion of residential mortgage lending activity, but it does not include every institution, every loan product, or every mortgage market transaction.

Many FHLBank Lenders Fall Outside HMDA’s Reporting Framework

Understanding these limitations is particularly important when evaluating the FHLBank System because its membership is dominated by community-based financial institutions, the very lenders most likely to fall below HMDA’s reporting thresholds or engage in housing finance activities that HMDA does not capture.

The FHLBanks are member-owned cooperatives chartered by Congress to provide reliable liquidity to member commercial banks, credit unions, insurance companies, savings institutions, and community development financial institutions (CDFIs). The System serves members of all sizes, but membership is overwhelmingly concentrated among smaller depository institutions. An analysis published in April 2026 showed that 96.5 percent of FHLBank depository members have $10 billion or less in assets, with many members holding less than $1 billion, or even $100 million, in assets.[2]

Small community banks and credit unions often originate mortgage loans that meet customer and local market needs but do not originate mortgages at volumes that trigger HMDA reporting thresholds.

For closed-end mortgages – traditional home purchases, refinances, and fixed-term home equity loans that are repaid over a fixed time period – an institution is required under the HMDA rule (last updated in 2022) to report if it originates at least 25 such loans in each of the two preceding calendar years. For home equity lines of credit (HELOCs), reporting is required only if an institution originates 200 or more of these open-end credit products in each of the two preceding calendar years.[3]

A small community lender may make a meaningful number of mortgage loans within its local market while still falling below these thresholds. According to FHFA’s National Mortgage Database (NMDB), the average mortgage loan amount in the third quarter of 2025 was $371,000.[4] At that average loan size, an institution would need to originate roughly $9.3 million in each of the two preceding calendar years in order to trigger the HMDA reporting threshold (25 x $371,000 = $9.275 million). For many smaller community financial institutions, particularly those serving rural or niche markets, that represents a substantial level of mortgage lending activity, and in some cases exceeds the total assets of the smallest FHLBank members. Thus, it is unsurprising that not all FHLBank members appear in the HMDA database. Small depository lenders play an important role in financing homeownership and community investment, often in markets overlooked by larger national financial institutions, even if they are not high-volume single-family mortgage originators.

It is also important to recognize that HMDA measures mortgage origination activity, but not the size or composition of an institution’s mortgage portfolio. A financial institution may provide significant funding to housing and mortgage markets through a portfolio of residential mortgages but not report to HMDA. If an institution does not originate closed-end mortgages or HELOCs above the reporting threshold, mortgage purchase activity will not appear in the HMDA data.

The key point is straightforward: absence from HMDA does not mean absence of housing finance activity. Many institutions that do not appear in HMDA continue to provide essential mortgage credit, liquidity, and financing that supports homeownership, rental housing, and the communities they call home.

The FHLBanks Support Mortgage Origination Through Their Acquired Member Asset Programs

The FHLBanks’ Acquired Member Asset (AMA) programs – including Mortgage Partnership Finance (MPF), Mortgage Purchase Program (MPP), and Mortgage Asset Program (MAP) – support housing finance by purchasing eligible single-family mortgage loans from participating financial institutions (PFIs). These programs provide liquidity that helps FHLBank members recirculate capital, manage prepayment and interest rate risk, and continue originating mortgages to meet the needs in their communities.

AMA programs allow member institutions to:

- Sell eligible whole mortgage loans.

- Free up balance sheet capacity and regulatory capital.

- Manage interest rate and concentration risk.

- Originate additional loans to serve their communities.

An internal analysis by the Federal Home Loan Bank of Chicago illustrates why HMDA data alone understates the housing finance support provided by the FHLBanks and their members. Examining HMDA data from 2020 through 2024, FHLBank Chicago found that 66 percent to 78 percent of active MPF PFIs appeared in the HMDA database. Conversely, 22 percent to 34 percent of active PFIs – members actively originating and selling mortgages through the MPF program – did not appear in the HMDA database.

Put differently, relying on HMDA data alone can overlook more than one-third of members participating in FHLBank AMA programs, greatly understating member and the FHLBank support for housing finance.

Housing Finance Extends Beyond Single-Family Mortgage Origination

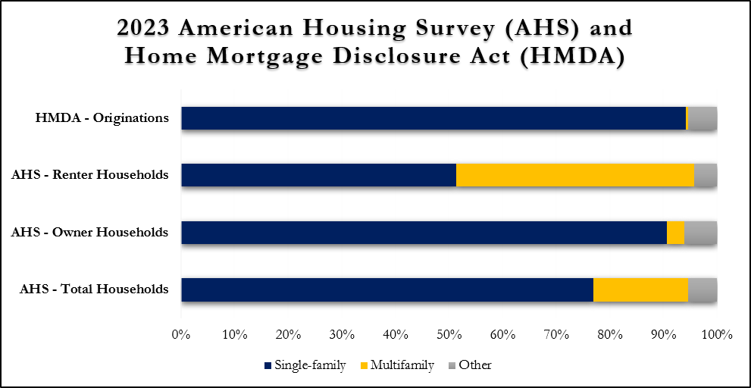

Another limitation of relying on HMDA data to identify institutions supporting housing finance is that HMDA only captures a portion of the housing finance ecosystem. HMDA data is primarily single-family mortgages, yet many FHLBank members specialize in multifamily lending or commercial real estate (including mixed-use) lending rather than single-family mortgage origination.

The 2023 American Housing Survey (AHS) shows that more than one-third of U.S. households are renters. Thus, financing for rental properties is critical to national housing markets and housing supply.[5] While HMDA does include some multifamily lending activity, reporting requirements are linked to institutional coverage and transaction volume thresholds. The Consumer Financial Protection Bureau reports that from 2018 to 2023 less than 1 percent of loans in HMDA were for multifamily properties, despite over 44 percent of rental units in the 2023 AHS being in multifamily properties.[6] Figure 1 compares coverage in HMDA and the AHS. Clearly, lenders focused on affordable multifamily rental properties, including small multifamily properties with 5–49 units, are not well represented in HMDA despite accounting for almost half of the U.S. rental housing stock.

Therefore, it is neither fair nor accurate to conclude that FHLBank members absent from HMDA are not supporting housing finance in the U.S.

Figure 1 – HMDA: A Snapshot, Not a Comprehensive Measure of All Mortgage Activity

Figure 1 – HMDA: A Snapshot, Not a Comprehensive Measure of All Mortgage Activity

Housing Finance Has Always Been Central to FHLBank Liquidity

Finally, and importantly, the connection between the FHLBanks and housing finance has never been solely based on loan origination. Since the System’s founding 94 years ago, collateral has been the key element linking FHLBank liquidity to its housing mission.

To obtain funding from an FHLBank, members must pledge eligible collateral. Collateral eligibility is set by Congress, and pledged collateral is overwhelmingly real estate related. As discussed in the March 2026 policy brief, Collateral Is Foundational, single-family whole mortgage loans account for roughly one-half of pledged collateral , and over 96 percent of pledged collateral is backed by real estate assets.[7]

According to the Urban Institute, banks, credit unions, and other portfolio lenders held approximately $2.7 trillion in residential (first lien) mortgages as of Q3 2025.[8] At the same time, more than $1.8 trillion in single-family residential mortgages were pledged to the FHLBanks as collateral, meaning roughly two-thirds of the residential home mortgages held in lenders’ portfolios are pledged to the FHLBanks for liquidity.[9]

Whether members originate single-family mortgages, originate multifamily loans, provide homeowners liquidity through HELOCs, or provide funding to originators by purchasing mortgages, FHLBank members support the same fundamental mission: supporting housing finance and community investment.

When a family purchases a home or a developer embarks on a new rental housing project, both need the services of an underwriter, an originator, and a funder, and the FHLBanks and their members provide support at every stage of the housing finance process.

The implication is straightforward. HMDA is an important mortgage disclosure dataset, but it is not a measure of the full housing finance ecosystem. The FHLBanks’ connection to housing finance extends well beyond the mortgages reported under HMDA. Through reliable, collateralized liquidity and mortgage purchase programs, the FHLBanks enable thousands of member institutions—particularly community-based lenders—to provide the financing that supports homeownership, affordable rental housing, and resilient communities across the United States.

[1] https://www.bloomberg.com/news/articles/2023-10-20/savvy-financiers-tap-billions-meant-for-mortgages-from-1-4-trillion-fhlb-system?embedded-checkout=true

[2] https://fhlbanks.com/policy-brief-as-designed-the-fhlbanks-execute-their-mission-day-in-and-day-out/

[3] https://www.consumerfinance.gov/rules-policy/final-rules/regulation-c-home-mortgage-disclosure-act/

[4] https://www.fhfa.gov/data/dashboard/nmdb-new-residential-mortgage-statistics

[5] https://www.census.gov/programs-surveys/ahs/data/interactive/ahstablecreator.html?bygroup1=COL_TENURE

[6] https://files.consumerfinance.gov/f/documents/cfpb_2023-mortgage-market-activity-and-trends_2024-12.pdf

[7] https://fhlbanks.com/policy-brief-for-the-fhlbanks-collateral-is-foundational/

[8] https://www.urban.org/sites/default/files/2026-03/February%20v3.pdf

[9] https://www.fhlb-of.com/ofweb_userWeb/resources/2024Q4CFR.pdf